How To Add a Name to a Deed: A 5-Step Guide

Get the legal advice you need without the hourly legal fees

Key Takeaways

- Adding a name to a deed usually involves creating a new deed with both names on it.

- A Quitclaim deed is one of the most common options.

- How you hold the title (not just whose name is on it) affects legal rights and inheritance.

- Check with your mortgage lender before making changes.

- Rules and forms vary by state and county.

Adding a name to your home’s deed is a common step for many couples. Maybe you just got married. Or maybe you’re just now getting your paperwork in order. Getting it right now can save you stress and confusion later.

The process is straightforward, but you’ll need to make a few key decisions along the way. When adding a name to your deed, you’ll want to make sure ownership is clear and that things can transfer smoothly in the future. That includes choosing how the title is held and understanding what that means for your family. Getting legal advice through a LegalShield® Membership is a good idea to ensure that you understand the right steps to take.

5 steps to add your spouse to your property deed

This is one of those processes where the details matter — a lot. Most states follow a similar set of steps: You prepare a new deed, sign it properly, and file it with your county. But the exact forms, fees, and requirements vary, so it’s always smart to double-check your local rules and have a lawyer review your documents.

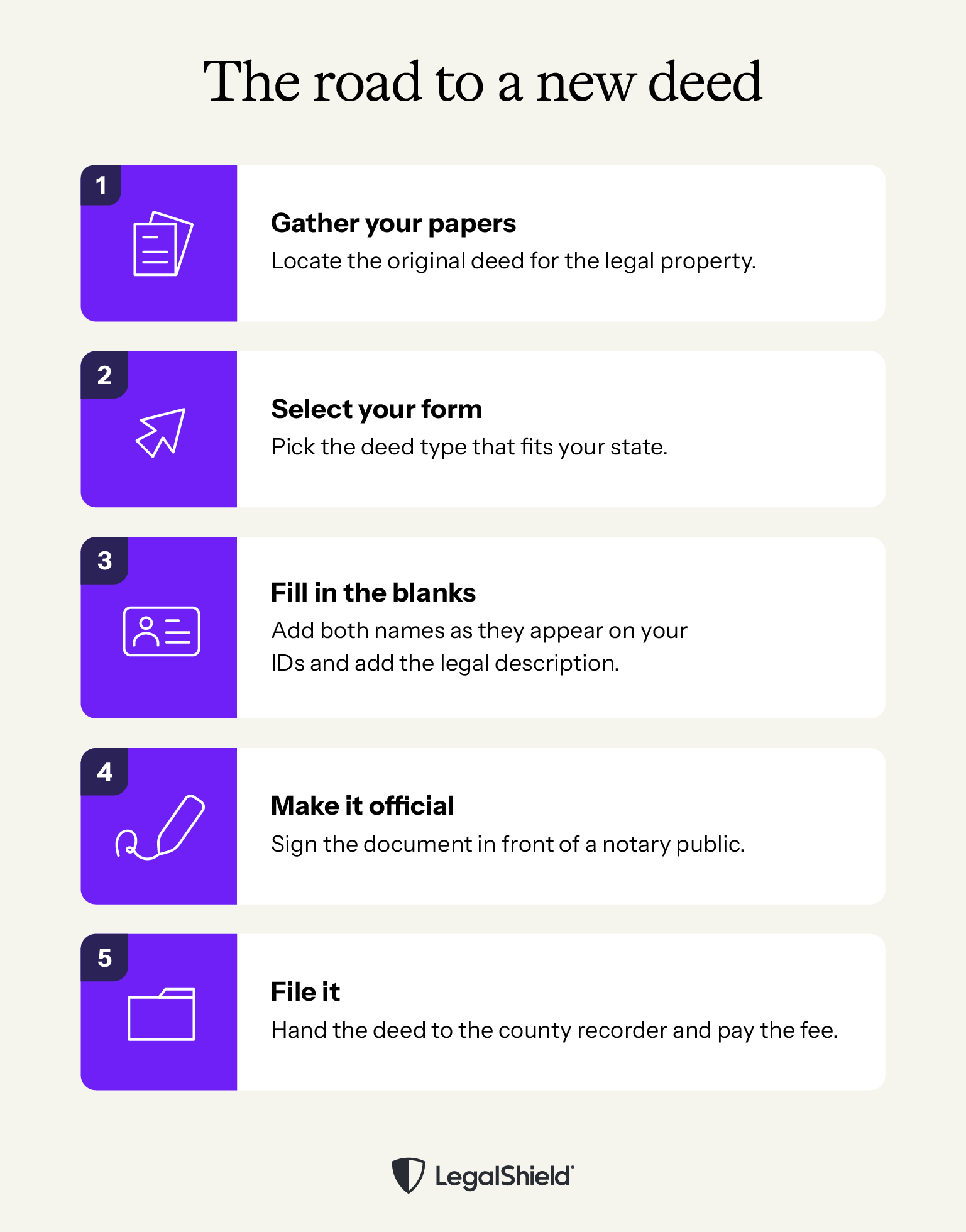

Step 1: Find your current deed

Start by locating your existing deed. This document includes the full legal description of the property. That’s required for any new deed.

You can usually find the deed with your closing paperwork. Or request a copy from your county recorder’s office. Some counties have deeds available online for free, or for a fee.

Step 2: Choose the right deed form

You’ve got options here. Many couples use a Quitclaim deed to add a spouse, but in some states a Grant deed or Interspousal Transfer deed may be more appropriate.

The right choice depends on your state laws and whether you want to include certain ownership guarantees.

Step 3: Complete the form carefully

Fill out the new deed with both your and the other person’s full legal names exactly as they appear on legal forms of ID. You’ll also need to choose how you want to hold the title. (For instance, joint tenancy with right of survivorship, which we’ll explain later.)

You’ll also need to provide the exact legal description of the property. You can find this on the previous deed. It is very important that the legal description from your original deed is exactly restated on the new deed. Don’t abbreviate or make any changes. If your original deed has a misspelling or something that does not seem correct, it’s best to consult with a lawyer on how to correct this.

Even small mistakes, like a typo or a missing detail, can cause delays.

Step 4: Sign the deed in front of a notary

Now you need a notary public to witness your signing of the completed deed. This is what makes the document legally valid and ready for recording.

Step 5: Record the deed with your county

Take the signed deed to your local county recorder’s office. You’ll pay a small filing fee and then the county will officially update the public record to reflect the new ownership.

Keep in mind that real estate laws vary by state and even county. For instance, some states will ask for extra forms, specific wording, or transfer tax disclosures. Others offer unique deed types or ownership structures that might fit your situation better.

Common types of deeds to use

When you’re adding a name to a deed, choosing the right type of deed is one of the most important choices you’ll make. Here’s a closer look at some of your options:

Quitclaim deed

To add a spouse, a quitclaim deed is the most common option. It transfers the ownership interest you have in the property to you and your spouse together,without making any guarantees about the title.

There’s no sale involved, so this is a quick, low-cost way to update ownership. That’s why spouses and family members use this type of deed so often.

Grant deed

A Grant deed offers a bit more protection than a Quitclaim deed. It generally guarantees that you haven’t already sold the property to someone else and that there are no undisclosed liens.

This type of deed is more common in certain states (like California). And it may be required, depending on local rules.

Interspousal Transfer deed

Interspousal Transfer deeds are available in some states. They sometimes offer tax advantages and simplified filing requirements. (That depends on local laws.)

If this option is available to you where you live, it can be one of the most efficient ways to add a spouse to your deed. Because the transfer happens directly between spouses, it usually involves less paperwork than a traditional sale and may be exempt from certain transfer taxes or reassessment, which can save time and money. In many cases, it’s a straightforward form that can be prepared and recorded without restructuring your mortgage or changing other terms of the loan.

General Warranty deed

A General Warranty deed gives you the most protection. It guarantees that the title is free of issues throughout the property’s entire history. This type of deed is pretty standard in home purchases..

Special Warranty deed

A Special Warranty deed falls somewhere in the middle in terms of title guarantees. It only guarantees that no title issues occurred during your period of ownership, not before. This type is more common in commercial transactions. But it still could make sense, depending on your state and situation.

Beneficiary (TOD) deed

Beneficiary deeds are also called Transfer-on-Death (TOD) deeds. They let you name who will inherit your home when you pass away — without adding them to the title right now. This means your spouse doesn’t have ownership rights during their lifetime, but the property transfers to them automatically after you die. That often avoids probate.

This can be a simple and low-cost option in states that allow it. But it offers less flexibility and control than shared ownership. And you’ll need to check your local laws, as TOD deeds aren’t available in every state.

Why you might want to add your spouse to the deed

Adding your spouse to your home’s deed can bring peace of mind and practical benefits.

One of the biggest reasons couples do this is to help avoid probate. If you own the property together in the right way (like joint tenancy with right of survivorship), ownership can pass directly to the surviving spouse. That avoids a long and often costly court process. It also makes your intentions for your home clear. And that can prevent confusion and disputes later.

Shared ownership can provide added protection for both partners because it clearly establishes shared ownership of the home. It also gives you some financial and legal benefits. Having both names on the deed can make it easier when you apply for things like a home equity line of credit (HELOC) or want to refinance your mortgage.

Ways to jointly hold the title

Adding a name to a deed is only part of the process. How you hold the title matters just as much. The ownership structure you choose determines your legal rights while you both own the home and what happens to the property if one of you passes away.

Choosing the right option can help you transfer property without probate. It also protects your interests and simplifies things for your family down the road. Here’s a look at your options:

Joint tenancy with right of survivorship

Joint tenancy is one of the most common options for married couples. In a joint tenancy with right of survivorship (JTWROS), you both own the property equally. If one of you dies, the other becomes the sole owner. That happens automatically. No probate required. However, the living spouse might choose to file a new deed removing the deceased spouse from the deed, making things easier when transferring the property at a later date.

Because it’s simple and effective, this setup is popular. But both of you have to agree to any major decisions related to the property, like selling or refinancing. It also means you both have an equal financial share — regardless of how much you each contributed.

Tenancy by the entirety

Tenancy by the entirety is a special kind of ownership that’s only available to married couples in certain states. It works a lot like joint tenancy. It has an automatic transfer to the surviving spouse. But it often adds more legal protections.

Where applicable, this structure can protect the property from the creditors of one spouse. It treats you and your spouse as a single legal entity. That can provide extra peace of mind, because a creditor cannot seize any property belonging to a person who owes them nothing. Availability and specific rules vary based on where you live.

Community property

In community property states, most property acquired during the marriage is considered jointly owned. That’s regardless of whose name is on the deed. And it usually means you and your spouse both have a 50 percent interest in the home.

Some community property states also give you a “community property with right of survivorship” option. This allows the property to pass automatically to the surviving spouse without probate.

Check with your mortgage company before you make any deed changes

Before you add a name to a deed, take a close look at your mortgage agreement. Most loans include what’s called a “due-on-sale” clause. This gives the lender the right to demand full repayment of your loan if the ownership of the property changes.

Transfers between spouses are very common, and in most circumstances, federal law prohibits mortgage lenders from activating “due-on-sale” clauses when your spouse or child becomes an owner of the property. But you should not assume you’re in the clear. Notify your lender ahead of time to prevent issues and surprises.

Also keep in mind that adding your spouse to the deed to property is not the same thing as adding your spouse to the mortgage. If you want them on the loan as well, you’ll usually need to refinance the loan. This will depend on your lender and loan terms.

Tax and cost considerations of deed changes

Affordable, not free — that’s the best way to describe the cost of adding a name to a deed. There are some small fees. And there can be tax implications, depending on your situation.

In many cases, transferring ownership to a spouse is treated differently from a typical home sale. That can help you avoid some taxes. But some states or localities might still require transfer forms or disclosures. And in some rare cases, the change could be seen as a gift for tax purposes. Rules vary widely here. So speak with a CPA or lawyer if you’re unsure.

Here’s a look at some costs to plan for as you add a name to a deed:

- Notary fees: These are typically between $5 and $30, depending on your state’s rules.

- County recording fees: This also varies wildly by location, amount of pages, legal tracts and other factors, but it’s usually going to cost you $20 to $100.

- Deed preparation costs: This is free if you do it yourself. If you use a third party, such as a lawyer or other service, you will pay an hourly or fixed fee, which varies.

- Transfer taxes or exemptions: Many states will waive these for transfers between spouses (but not necessarily all transfers between family members). But you may still have to file some exemption paperwork or cite your exemption on the deed.

- Title company or legal review: This might add cost, but it can help you avoid mistakes that lead to bigger expenses later on.

Upfront costs are pretty low,but mistakes in a deed can be very expensive to fix. Taking a little extra time or getting guidance from a lawyer can save you a lot of trouble later.

How a lawyer can help you

A small mistake in wording or filing can create big problems later, especially when you try to sell the home or transfer ownership.

A LegalShield® Membership gives you access to a law firm for around $1 a day. With a plan, you can connect with a provider lawyer who can answer your questions, review your documents, and help you move forward with confidence without the high hourly fees.

A provider lawyer can help you choose the best way to hold title. Whether it’s joint tenancy, tenancy by the entirety, or another structure, the right choice can help your family avoid probate and reduce legal headaches.

Getting the right guidance now can save you and your family stress and money later.

Get help protecting your assets and loved ones with LegalShield

Knowing how to add a name to a deed is just one step. The real goal is making sure your home and the people you care about are protected in the long run.

With a LegalShield Personal Plan, you can talk to a provider lawyer about real-life situations — like reviewing your deed, understanding the best way to hold title as a married couple, or getting guidance about estate planning.

Explore LegalShield Personal Plans to get affordable guidance when you need it. A provider lawyer can review your documents, answer your questions, and help you take the next step with clarity.

Frequently asked questions

Is adding a spouse to a deed considered a gift?

In some cases, adding a spouse can be considered a gift of an ownership interest in the property. But transfers between spouses are often treated differently for tax purposes. And they may qualify for exemptions under federal and/or state law. Even with an exemption, you may still need to file certain forms or disclosures depending on where you live. Check with a tax professional or lawyer to avoid surprises.

What are the disadvantages of adding someone to a deed?

One disadvantage of adding someone to a deed is that you’re giving that person legal ownership rights. That means they have to agree to major decisions like selling or refinancing the property. You might also expose your home to that person’s creditors or similar legal problems. And in some cases, your taxes might become more complex.

Should you add your spouse to your deed?

For many couples, the answer is yes, you should add your spouse to your deed. But really, it depends on your goals. Adding a spouse to a deed can help you skip probate, make inheritance simpler, and reflect your shared ownership. But it’s not always the best option for every situation — especially if you have concerns about taxes, debt, or long-term planning.

Do I need a lawyer to add a name to a deed?

You don’t always need a lawyer to add a name to a deed. Some people do it themselves. But small mistakes can cause delays, legal issues, or problems if you want to sell the home later. A lawyer can make sure the document is accurate, complies with state laws, and reflects your intentions.

What is the best way to hold title as a married couple?

The best option depends on your state and your priorities. Many couples choose joint tenancy with right of survivorship or tenancy by the entirety. Both allow the property to pass automatically to the surviving spouse. In community property states, though, other options can provide tax benefits. Speaking with a lawyer can help you make the right call.

LegalShield® is a trademark of Pre-Paid Legal Services, Inc. (“LegalShield”). LegalShield provides this blog as a public service and for general information only. The information made available in this blog is meant to provide general information and is not intended to provide legal advice, render an opinion, or provide a recommendation as to a specific matter. The blog post is not a substitute for competent legal counsel from a licensed professional lawyer in the state or province where your legal issues exist, and you should seek legal counsel for your specific legal matter. All information by authors is accepted in good faith. However, LegalShield makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of such information. The materials contained herein are not regularly updated and may not reflect the most current legal information. No person should either act or refrain from acting on the basis of anything contained on this website. Nothing on this blog is meant to, or does, create an attorney-client relationship with any reader or user. An attorney-client relationship may be formed only after the execution of an engagement letter with an attorney and after that attorney has confirmed that no conflicts of interest exist. Nothing on this website, or information contained or transmitted by this website, is intended to be an advertisement or solicitation. Information contained in the blog may be provided by authors who could be a third-party paid contributor. LegalShield provides access to legal services offered by a network of provider law firms to LegalShield members through membership-based participation. LegalShield is not a law firm, and its officers, employees or sales associates do not directly or indirectly provide legal services, representation, or advice.

Get the Answers You Need, When You Need Them

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.