LLP vs. LLC: Key Differences and How To Choose

This post was originally published on September 17, 2021, and has been updated for accuracy, comprehensiveness, and freshness on March 24, 2026.

- LLCs are flexible. They work for solo or multi-owner businesses, and let you choose how you're taxed.

- LLPs require two or more partners. Many states limit LLPs to licensed professionals, like lawyers, accountants, and architects.

- The right choice depends on your business type and the number of owners.

Figuring out a business structure can feel overwhelming when all you really want is to get your business off the ground. One of the most common questions is the difference between an LLC and an LLP. When choosing between a limited liability company and a limited liability partnership, both offer protection, but they work in different ways. In this guide, we'll break down LLC vs. LLP and how to decide which is right for you.

What is an LLP?

A limited liability partnership (LLP) is a business entity formed by two or more owners in partnership with each other. LLPs are a common choice for people who want to pool their talents and resources while still shielding their personal assets and limiting their personal liability.

Unlike a general partnership, where there's no legal entity and each partner takes on unlimited liability, an LLP is an actual separate business entity that limits the personal liability of the partners involved in most states. Note that some states need at least one partner to have unlimited personal liability.

It's also worth noting that many states (including California, New York, and Nevada) only allow licensed professionals to form LLPs. Doctors, lawyers, accountants, and architects can typically create one, but a retail shop or tech startup might not be able to.

What is an LLC?

A limited liability company (LLC) is a business structure that protects your personal assets from business debts. LLCs work for almost any type of business, from freelancers and online stores to restaurants and construction companies.

You can set one up with just yourself or bring in multiple members, making it the go-to for solo entrepreneurs (something you can't do with an LLP).

They're easier and cheaper to form than corporations but offer many of the same protections, which is why they're one of the most popular choices for small business owners.

Key differences between LLP and LLC

The biggest differences between an LLC and an LLP (besides the need for at least one business partner to form an LLP) are how they're managed, the protection they offer owners, and how they're taxed. Depending on your business type and who's involved, any one of those could be the deciding factor.

Management structure

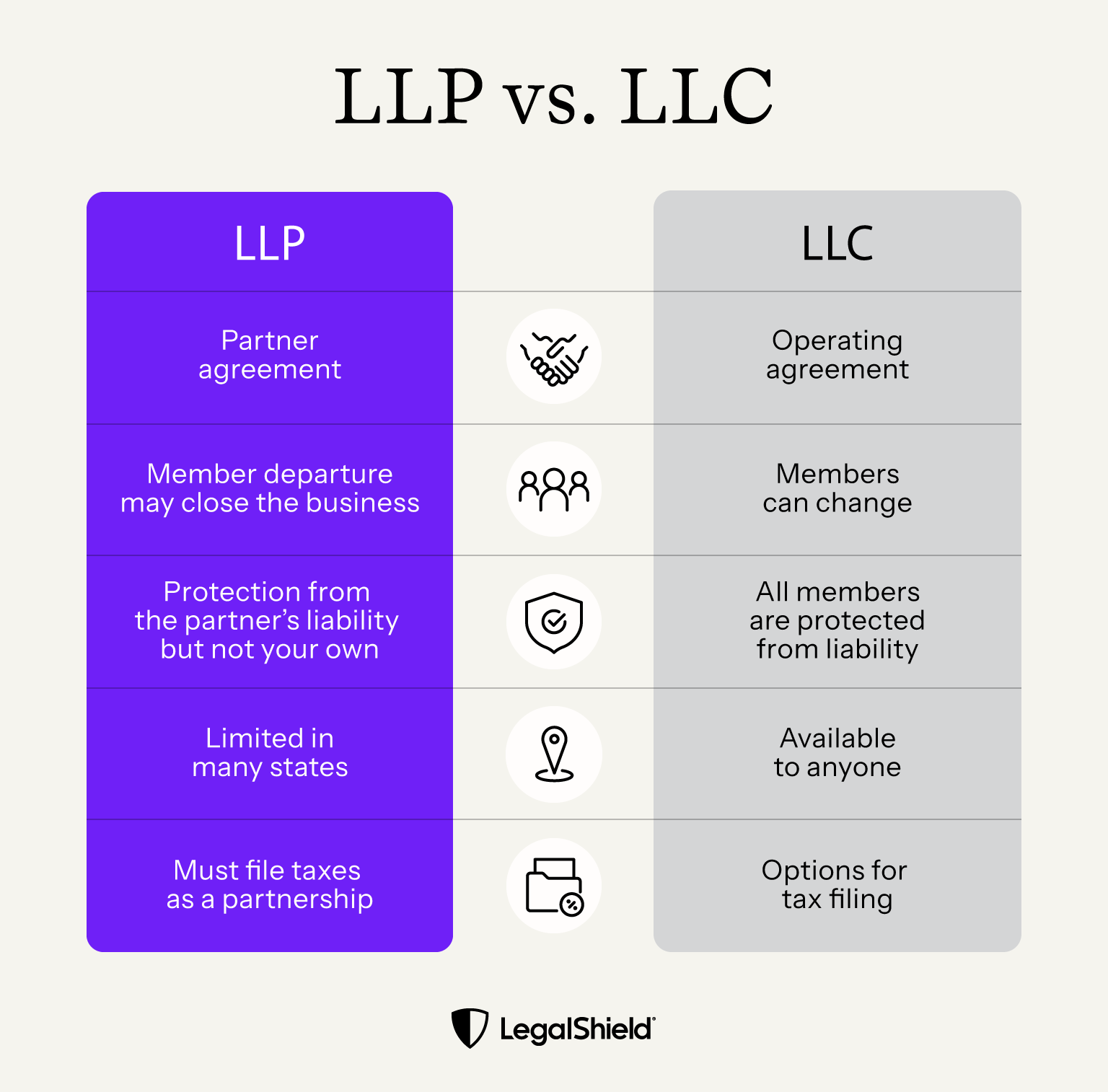

In an LLC, the operating agreement determines how you manage the business. It lays out who does what, how decisions get made, and how to make changes to the membership.

You can go with a member-managed setup where everyone has a say, or a manager-managed setup where one or a few people run things while the others stay hands-off. And if you're on your own, an LLC lets you keep full control as a single member.

In an LLP, a partnership agreement spells out each partner's role, how much money they put in, and how profits get split. One or more partners can choose to be a silent partner, letting the others handle the day-to-day.

One key difference: LLCs usually keep going even if a member leaves. But with some LLPs, a partner walking away can force the business to shut down, depending on what the partnership agreement says and what your state requires.

Liability protection

Protecting your personal assets is one of the biggest reasons to form a business entity in the first place. Both LLCs and LLPs offer liability protection, but they do it differently.

With an LLC, your personal assets (home, car, savings) are generally safe from business debts and lawsuits. As long as you keep your personal and business finances separate and don't do anything illegal, creditors can't come after your personal stuff.

An LLP helps protect you from your partners' mistakes but not your own. If you mess up on a client's case or account, you're personally on the hook. Depending on your state, partners may still share liability for the overall debts of the business.

Tax benefits

Both LLCs and LLPs are pass-through entities, meaning profits and losses show up on your personal tax return instead of a separate business return. That helps you avoid paying taxes twice.

The difference is in your options. LLPs can file taxes only as partnerships. LLCs get to choose — you can be taxed as a sole proprietorship, partnership, or corporation, depending on what saves you the most money.

If you're thinking about electing corporate taxation, keep in mind that it comes with "double taxation" (the business pays taxes on its profits, and then you pay taxes again on what you take out). A tax professional can help you figure out if that trade-off makes sense.

Eligibility and restrictions

Not everyone can form both types of entities. Here are the primary restrictions to keep in mind:

- LLPs are limited in many states: States like California, New York, and Nevada only allow licensed professionals (such as lawyers, CPAs, doctors, and architects) to form LLPs. If your business isn't a licensed profession, an LLP may not be an option.

- LLCs are available to nearly anyone: Most states allow any type of business to form an LLC, with very few restrictions. Check your state for any exceptions to forming an LLC.

- LLPs always require two or more partners: If you're starting a business by yourself, an LLP isn't an option. You would need to go with a single-member LLC instead.

Advantages and disadvantages of LLCs and LLPs

Both structures have tradeoffs. Here's a look at the pros and cons of each.

Pros and cons of LLCs

LLCs come with a lot of upside, but there are a few trade-offs to keep in mind.

Pros:

- Available to almost any type of business in any state

- Allows single-member or multiple-member ownership

- Flexible tax options

- Strong liability protection for all members

- The business can continue if a member leaves

Cons:

- Self-employment taxes apply to all members in most cases

- Some states charge annual fees or franchise taxes for LLCs

- Operating agreements can get complex with multiple members

- Investors may prefer other entity types

If you want to dig deeper, check out the full breakdown of the pros and cons of an LLC.

Pros and cons of LLPs

LLPs are made for professional partnerships. However, they come with some limitations depending on your state.

Pros:

- Partners aren't liable for each other's negligence or malpractice

- Pass-through taxation avoids double taxation

- Flexible management through partnership agreements

- Well-suited for professional firms where each partner manages their own clients

Cons:

- Not available for all business types

- Requires at least two partners

- Liability protection varies by state

- May dissolve if a partner leaves, depending on the agreement and state law

How to choose between an LLC and an LLP

Choosing between an LLC and LLP comes down to a few main questions: How many owners does your business have? What industry are you in? What does your state allow?

Choose an LLC if:

- You're starting a business on your own

- You want flexibility in how you're taxed

- Your business isn't in a licensed profession

Choose an LLP if:

- You're in a licensed profession and want to partner with colleagues

- You want protection from your partners' mistakes

- Your state allows LLPs for your industry

How to form an LLC or an LLP

The formation process is similar for both, but there are some differences.

How to form an LLC

- Choose a business name that's available in your state.

- File Articles of Organization with your state's Secretary of State.

- Draft an operating agreement outlining member roles, ownership percentages, and management structure.

- Apply for an EIN through the IRS.

- Register for any required state or local licenses.

If you need help getting started, learn how to start an LLC step by step.

How to form an LLP

- Confirm your profession qualifies (many states limit LLPs to licensed professionals).

- Choose a business name (most states require "LLP" in the name).

- File a registration or certificate of LLP with your state.

- Pay the filing fee.

- Draft a partnership agreement covering each partner's role, financial contributions, and profit-sharing.

- Apply for an EIN through the IRS.

With a LegalShield business plan, you can get a consultation with a provider lawyer to talk through partnership agreements, operating agreements, and which business structure makes the most sense for your situation.

Once you choose between LLC or LLP, get peace of mind with LegalShield

Choosing the right structure and setting it up correctly is where a lawyer can help the most. With a LegalShield business plan, you get consultations with a provider lawyer who can help with things like reviewing your operating agreement or partnership agreement before you sign.

You don't have to figure it out alone. Whether you need a contract reviewed before you sign, help collecting on a late invoice, or a lawyer to step in when a business dispute comes up, LegalShield's business legal plans put an experienced lawyer in your corner for an affordable monthly fee.

Frequently asked questions

Which is better, LLC or LLP?

For most small businesses and solo entrepreneurs, an LLC can be the better fit because of its flexibility and availability. LLPs work well for licensed professionals who want to partner together while staying protected from each other's liability.

Can I convert from an LLP to an LLC?

In some states, you can convert an LLP to an LLC by filing a conversion document. Other states require completely dissolving the LLP and forming a new LLC. Talking to a lawyer before starting the process is a wise idea to make sure you don't miss any steps or create unexpected tax issues.

Is an LLP or LLC easier to set up?

LLCs tend to be slightly easier because they're available in all states and don't have professional licensing requirements. LLPs may require extra steps, such as verifying that your profession qualifies, meeting state-specific partnership rules, and drafting a partnership agreement.

LegalShield® is a trademark of Pre-Paid Legal Services, Inc. (“LegalShield”). LegalShield provides this blog as a public service and for general information only. The information made available in this blog is meant to provide general information and is not intended to provide legal advice, render an opinion, or provide a recommendation as to a specific matter. The blog post is not a substitute for competent legal counsel from a licensed professional lawyer in the state or province where your legal issues exist, and you should seek legal counsel for your specific legal matter. All information by authors is accepted in good faith. However, LegalShield makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of such information. The materials contained herein are not regularly updated and may not reflect the most current legal information. No person should either act or refrain from acting on the basis of anything contained on this website. Nothing on this blog is meant to, or does, create an attorney-client relationship with any reader or user. An attorney-client relationship may be formed only after the execution of an engagement letter with an attorney and after that attorney has confirmed that no conflicts of interest exist. Nothing on this website, or information contained or transmitted by this website, is intended to be an advertisement or solicitation. Information contained in the blog may be provided by authors who could be a third-party paid contributor. LegalShield provides access to legal services offered by a network of provider law firms to LegalShield members through membership-based participation. LegalShield is not a law firm, and its officers, employees or sales associates do not directly or indirectly provide legal services, representation, or advice.

LegalShield is a trademark of Pre-Paid Legal Services, Inc. (“LegalShield”). LegalShield provides this blog as a public service and for general information only. The information made available in this blog is meant to provide general information and is not intended to provide legal advice, render an opinion, or provide a recommendation as to a specific matter. The blog post is not a substitute for competent legal counsel from a licensed professional lawyer in the state or province where your legal issues exist, and you should seek legal counsel for your specific legal matter. All information by authors is accepted in good faith. However, LegalShield makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of such information. The materials contained herein are not regularly updated and may not reflect the most current legal information. No person should either act or refrain from acting on the basis of anything contained on this website. Nothing on this blog is meant to, or does, create an attorney-client relationship with any reader or user. An attorney-client relationship may be formed only after the execution of an engagement letter with an attorney and after that attorney has confirmed that no conflicts of interest exist. Nothing on this website, or information contained or transmitted by this website, is intended to be an advertisement or solicitation. Information contained in the blog may be provided by authors who could be a third-party paid contributor. LegalShield provides access to legal services offered by a network of provider law firms to LegalShield members through membership-based participation. LegalShield is not a law firm, and its officers, employees or sales associates do not directly or indirectly provide legal services, representation, or advice.

How To Start an LLC in Michigan in 7 Steps

LLC vs. Corporation: Key Differences + Which To Choose for Your Business