Incorporation turns your business into a separate legal entity. A corporate structure protects your personal assets, offers tax advantages, builds long-term stability, and opens the door to more funding opportunities. However, corporations are extremely complicated and may not be right for small businesses.

As a business owner, protecting what you’ve built matters. You want to keep both your company and your personal assets safe. You also want to reduce risks and create a strong future for your company. If you’re wondering how to do that, incorporating your company might be the answer.

Incorporation is the legal process of turning a business into a “legal person” that’s separate from you. An incorporated business can own property, pay taxes, and sign contracts under its own name. It can also borrow money and be legally responsible for itself.

That separation helps protect you from personal liability if your business runs into legal or financial problems. Instead of everything falling on you, the business handles its own obligations, so it’s good for both you and your business.

Let’s look at the many advantages of incorporation. Understanding them can help you decide if incorporating your business is right for you.

1. Protect your personal assets with incorporation

Liability protection means that business creditors and people bringing lawsuits can't come after you personally. That’s a great way to protect yourself, and you can get it through incorporation.

When businesses get into trouble, their owners could lose everything. But, there's a way to keep that from happening. Incorporating and operating your business according to law creates a “corporate veil.” This legal barrier usually keeps your personal assets safe, including:

Your main home and other real estate

Personal bank and investment accounts

Personal vehicles and boats

Retirement accounts

Personal property

Suppose someone sues your corporation. You shouldn’t lose your home and other personal belongings. Only your business should be responsible, not you.

2. Maximize tax savings and deductions

Incorporation lets businesses choose their tax structure, which could help them select the most beneficial one for their situation.

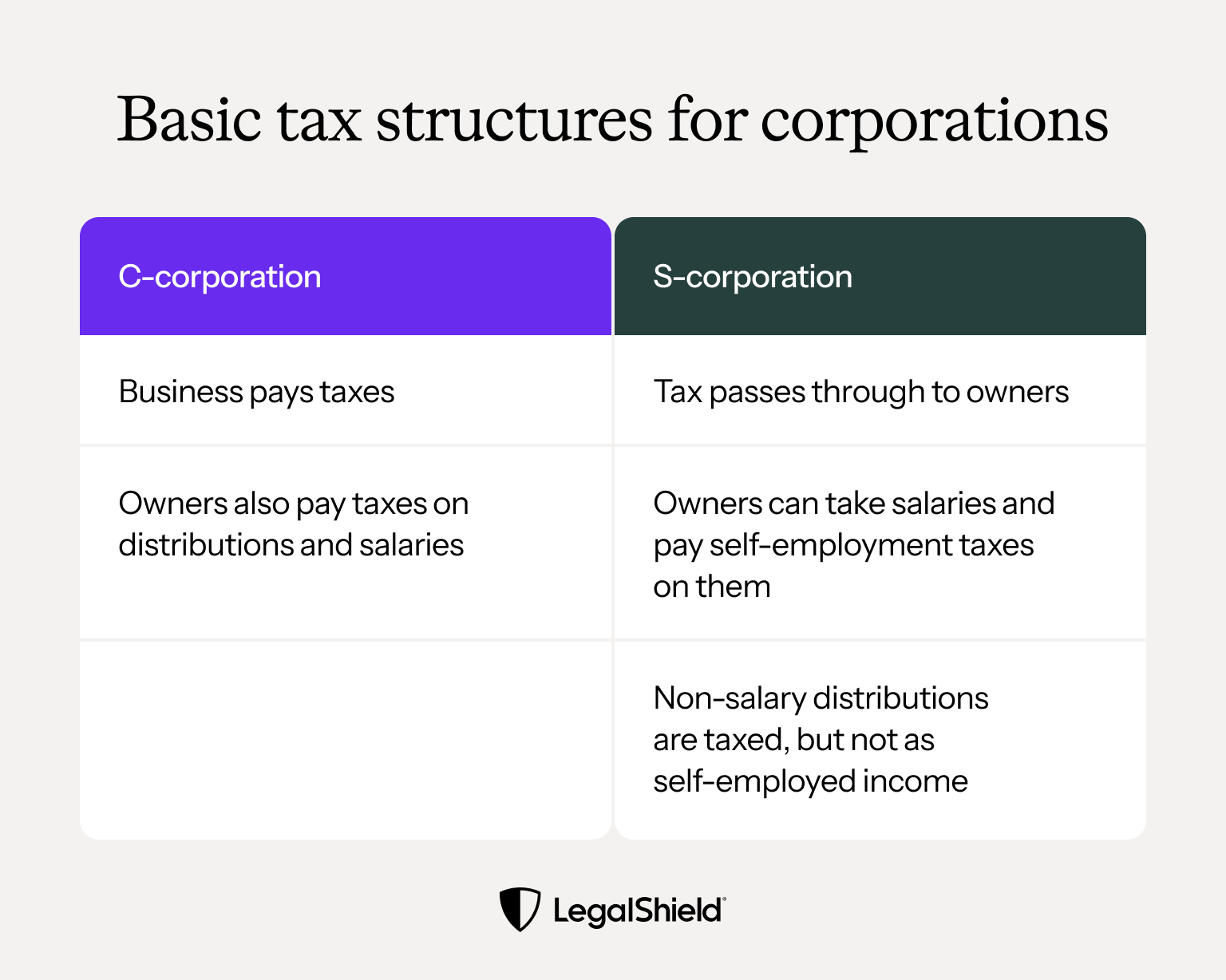

Let’s look at some corporate tax structures:

C-corporation: Pays its own taxes, corporate tax rates might be lower

S-corporation: Owners pay tax on profits themselves, avoiding double taxation

Disregarded entity: This tax structure is only available to limited liability companies (LLC). If you want to read more about LLC tax classifications, go

Take advantage of deductions and retained earnings

Another benefit of forming a corporation for tax purposes is that you can deduct lots of business expenses. That means a lower taxable income and an improved cash flow. Those deductions may include:

Employee health insurance premiums

Business travel and lodging

Advertising and marketing costs

Equipment and office supplies

Also, you can leave profits in the company instead of taking them as personal income. Keeping those retained earnings in your company is a great strategy for delaying personal income tax liabilities. It also gives you funds for growing your company.

3. Access capital and fuel business growth

At some point, your business will probably need to borrow money or raise capital. Banks and other lenders may seek stock as collateral. Investors may want stock in return for their investment. Corporations have more formal recordkeeping and the ability to issue different types of stock, which may be more enticing to banks and investors.

4. Ensure business continuity and perpetual existence

A corporation has a life of its own. If an owner leaves, retires, or passes away, the business can keep operating. Ownership changes don’t necessarily mean the company pauses or dissolves.

Business continuity is important because it could help you:

Reduce financial losses

Protect employees

Identify and prepare for risks

Protect your company’s reputation

Build customer trust

Reassure vendors

Incorporating means ownership changes don’t have to affect the company. It makes long-term planning easier because the business can last even without your involvement.

5. Transfer ownership without interrupting business

Seamless transfers can prevent lots of problems. Due to a corporation’s recordkeeping requirements, stock transfers are very formal and should be well-documented. This can prevent ownership questions down the line.

You might also want to pass company ownership to your children. You can use a Will or Trust to transfer your shares of stock. You also may be able to prepare a Transfer on Death (TOD) to leave them your shares and have them transfer without probate.

Key considerations before you incorporate

It’s important to weigh the pros and cons of incorporation before you make a decision. We’ve talked about why you should incorporate your small business, but let’s look at some possible concerns:

State filing fees for corporations can be high

You’ll have to file annual reports and pay a yearly renewal fee

Procedures are more formal than with other business structures; for example, you’ll need to hold corporate meetings and keep official minutes

Stock transfers and stock certificates must be recorded

You’ll need many additional levels of ownership and operating management, such as Shareholders, Board of Directors, and Officers

How to get professional help with incorporation

Incorporation is a great way to protect yourself and your company. The benefits can make the extra responsibilities worth it. Deciding to incorporate is a big decision, and you may want to ask a lawyer for advice.

LegalShield® Business Plans make it easy for you to get solid legal advice for a reasonable price. Your membership gives you access to a provider law firm for document reviews, contract concerns, and more. Get the guidance you need to start protecting your business today.

Frequently Asked Questions

It can be, depending on your purpose and the needs of your business. Look at the pros and cons for your specific situation before you decide. Asking a lawyer for advice is probably a good idea.

The biggest difference is how the business is run. LLCs are less formal and the law allows flexibility on structure and requirements. Corporations have stricter management rules and some things, like annual meetings, are required by law.

You don’t need a lawyer to incorporate, but legal guidance can help. A lawyer can help you decide if it’s the right business structure for you. Their advice can help you avoid costly mistakes.

The process of incorporation can take a few days or a few weeks. The timing depends on your state and when you submit all the required documents. You may be able to pay a fee for faster filing.

Yes, you can incorporate in another state. Many business owners register in their home states, and if doing business in other states, can register their business there as a foreign entity. Or you may choose to incorporate in a state known for its favorable business environment, such as Delaware or New York.

Incorporation is what you do to form a corporation. The corporation is the business entity you formed.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

Whether the goal is selling a company, bringing in a business partner, or passing it to a family member, the LLC ownership transfer often involves reviewing the LLC's operating agreement and the applicable state's rules.

•

11 min read

Author Name

,

Author Title

August 4, 2026

Small Business

6 min read

Trade Name: Definition, Examples, and How to Register a DBA

If you want to do business under a name that isn't your own legal name or your LLC's registered name, you need a trade name, also known as a doing business as (DBA) name.

•

6 min read

Author Name

,

Author Title

July 28, 2026

Small Business

5 min read

How To Create a Consulting Agreement for Your Business

A consulting agreement is a contract between a service provider, such as an independent contractor, and a recipient.

•

5 min read

Author Name

,

Author Title

July 28, 2026

Small Business

6 min read

What Is a Hold Harmless Agreement, and Do You Need One?

Hold harmless agreements can help reduce a business's liability by having signatories accept a certain amount of risk.

•

6 min read

Author Name

,

Author Title

July 9, 2026

Small Business

4 min read

How To Set Up an LLC in New York (and Why It's Unique)

Getting an LLC in New York generally involves choosing a business name, filing Articles of Organization with the New York Department of State, creating a written Operating Agreement, completing New York’s publication requirement, and handling tax and business setup steps, like getting an EIN.

•

4 min read

Author Name

,

Author Title

July 15, 2026

Small Business

5 min read

How To Franchise Your Business: A Six-Step Overview

Knowing how to franchise your business takes more than enthusiasm. It takes documented systems, legal preparation, and the right partners.

•

5 min read

Author Name

,

Author Title

June 17, 2026

Small Business

6 min read

How to Transfer Property to an LLC: A 5-Step Guide

In this guide, we walk you through how to transfer property to an LLC in just a few steps, along with key things to watch for so you can make this change with clarity and confidence.

•

6 min read

Author Name

,

Author Title

June 15, 2026

Small Business

9 min read

How To Create an Anonymous LLC: A Step-by-Step Guide to Business Privacy

It’s not available in every state, but certain jurisdictions allow you to form an LLC without listing members or managers in publicly searchable records.

•

9 min read

Author Name

,

Author Title

June 15, 2026

Thank you! You're subscribed!

Oops! Something went wrong while submitting the form.