Too many people make this call after it's already too late. Someone has just been in an accident and they're shaken, they've filed the claim, the car is at the shop, and they want to know if they did the right thing. Sometimes they did. But too often, they've already signed something they didn't fully understand and let the clock run out on options they didn't know they had.

This piece is about what comes after the accident.

We surveyed more than 1,000 Americans who filed an auto insurance claim in the past three years to understand what that process actually looked like. What came back was familiar.

Nearly 70% of drivers finalized their settlement within two weeks. Three-quarters (74%) said they felt comfortable with how it went. But roughly 37% ended up with a payout lower than they expected, or realized they had no idea whether what they accepted was fair. And almost half wish they'd done something differently before they signed.

The process moves fast by design, and most drivers don't realize they have the power to slow it down.

Key takeaways

Nearly 70% of drivers finalized their settlement within two weeks, 12% settled within 24 hours.

Nearly half of drivers (48%) wish they had done something differently when preparing their claim.

63% of drivers faced at least one unexpected cost beyond car repairs.

43% spent six or more hours on claim-related paperwork, phone calls, and follow-ups.

63% say they'd be more likely to involve a lawyer if legal access were bundled into a membership they already pay for.

What your insurer isn't telling you

Filing a claim sounds simple. You’ll call your insurer, submit some photos, and wait for a check. What the data shows looks different.

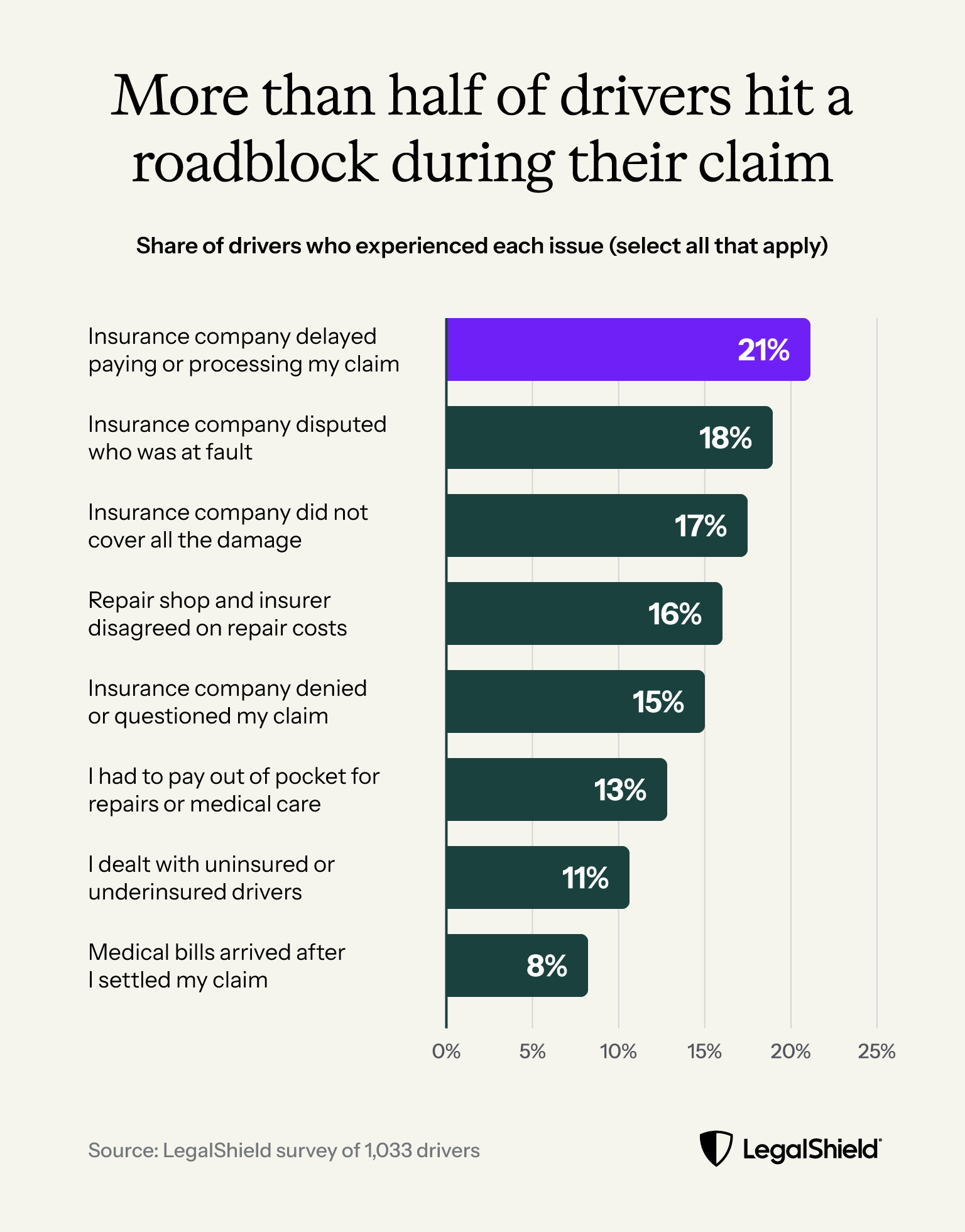

More than half (56%) of drivers in our survey experienced at least one problem during the claims process. These issues can vary a lot, and some can hit harder than others.

For example, a dispute over fault creates different complications than a repair estimate that comes in low, or a medical bill that surfaces three months after you've already settled. They create challenges at different points in the process, and most drivers are navigating it all without anyone in their corner.

A third of drivers said they could handle it themselves. Nearly a quarter didn't think they needed any guidance at all. It's a reasonable assumption. What the survey revealed is what happens when the process gets complicated, and the window for preparation has already closed.

Part of what makes that so costly, in my experience, is that most drivers don't know what they're entitled to ask for. Understanding what your insurer is actually required to do can change how the process goes.

What drivers can do before regrets set in

The number that stands out to me most: 12% of drivers signed off on their settlement within 24 hours of the accident, and nearly 70% were done within two weeks. I'm not saying fast is always wrong. But a settlement is more than just paperwork. It's often the end of your ability to come back and ask for more.

What most drivers don't realize is that signing quickly isn't required. In many states, drivers have the right to ask how a settlement figure was calculated, request an independent repair estimate, or simply wait. The process is designed to close fast. Understanding what you're giving up is your responsibility, and the timeline makes that hard.

And the survey confirmed that most people don't know that.

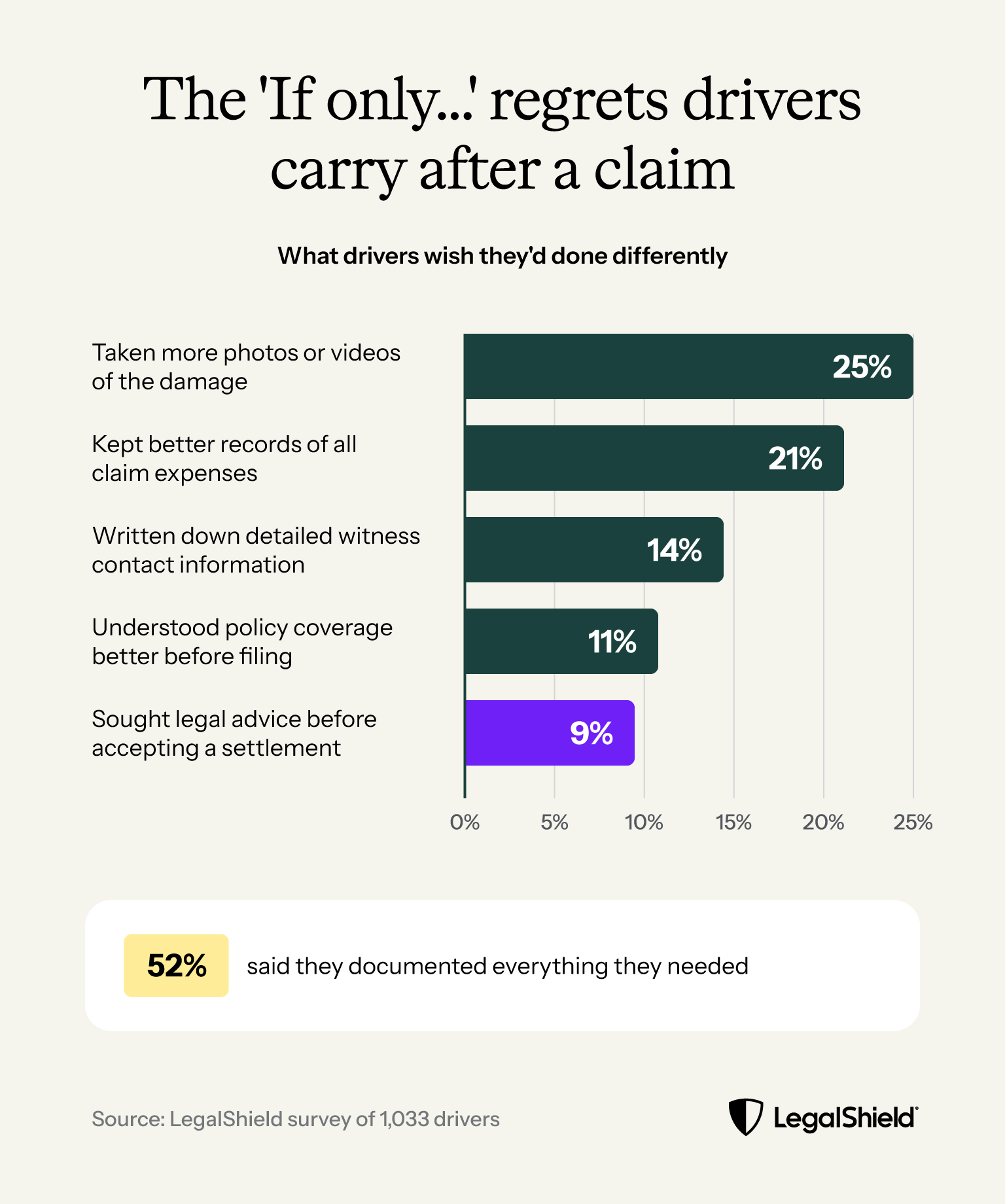

Nearly half of drivers (48%) said they wish they'd done something differently when preparing their claim. Twenty-five percent wish they'd taken more photos of the damage. Another 21% wish they'd kept better records of expenses. This kind of documentation is easy to gather at the scene and nearly impossible to recreate later.

Three in four drivers (74%) said they felt comfortable with the timing and information they had. But 37% got less than they expected or weren't sure whether what they accepted was fair. Fast timelines are part of how this happens. When a claim closes quickly, there's not much space to ask the questions you'd wish you'd asked, and the ones you didn't ask are the ones that tend to cost you.

What to do in the first 72 hours

The 72 hours after an accident is the moment to slow down. The legal process usually isn't urgent yet. But this is when details are clearest and the decisions feel small enough that people skip them. They're not small.

Here's what's worth doing in the first 72 hours before they respond to anything:

Photograph everything (the damage, the scene, any visible injuries) even if you think you already have enough photos. You probably don't.

Start a running log of every expense: rental car, prescriptions, missed work, anything connected to the accident. Bills have a way of arriving late.

Read your policy before you respond to anything. Know what your coverage actually includes before you accept a number that sounds reasonable.

Understand that a first offer isn't a final offer. In most states, you have the right to ask how it was calculated and take time before signing (though it's worth checking your state's specific rules).

Most people who skip these steps don't realize what they gave up. By the time they do, the claim is closed.

What the repair estimate doesn't include

By the time the repair is done, most people want to close the chapter. I get that. But this is when I'd tell anyone to stay alert, because the costs that follow an accident have a way of arriving quietly and late.

The repair estimate is the number everyone focuses on. It's usually not the biggest number by the time everything shakes out.

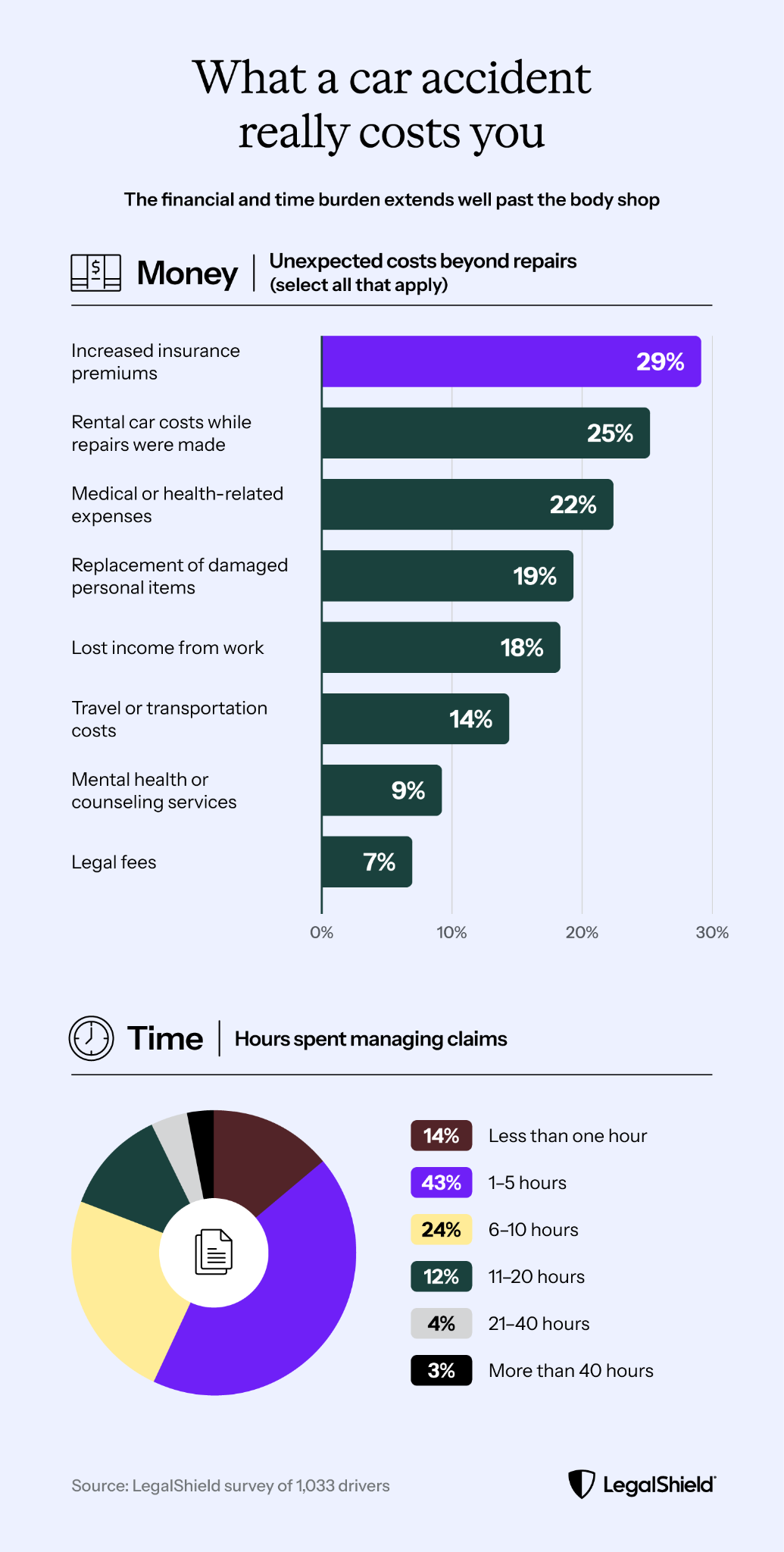

For 63% of drivers in our survey, at least one unexpected cost showed up after the fact. Higher premiums hit 29% (that bill doesn't arrive until the next renewal cycle). A quarter dealt with rental car costs while their vehicle was in the shop. Medical expenses came in for 22%, damaged personal property for (19%) and lost income (18%).

And then there's the time. Forty-three percent of drivers spent six or more hours on paperwork, phone calls, follow-ups, and adjuster back-and-forth alone. That's a part-time job nobody signed up for.

These costs don't announce themselves. The premium increase shows up on a renewal notice two months later, and medical bills can often arrive after you've already settled. You may also miss out on counting lost wages if no one told you to document them. By the time most people look for help, they've often already signed, and the window to push back is closed.

Most drivers aren't prepared for that shift, and the data backs it up.

Know your options before the claim closes

When something goes wrong with a claim, most people don't know where to start. The thing most drivers don't realize is that they have more options than they think, and most of them are available before thitngs get complicated.

A car insurance claim is a legal situation for some drivers and a paperwork exercise for others. A third thought they could handle it themselves. Nearly a quarter didn't think their situation was serious enough, and 22% were worried about cost.

But when a settlement offer comes in low or bills arrive after you've already signed, having a lawyer review the situation before you respond can make a real difference. That doesn't mean filing a lawsuit or hiring someone on retainer. It often means a second set of eyes on language most people aren't trained to read. Knowing when that kind of help makes sense is something most drivers only figure out in hindsight.

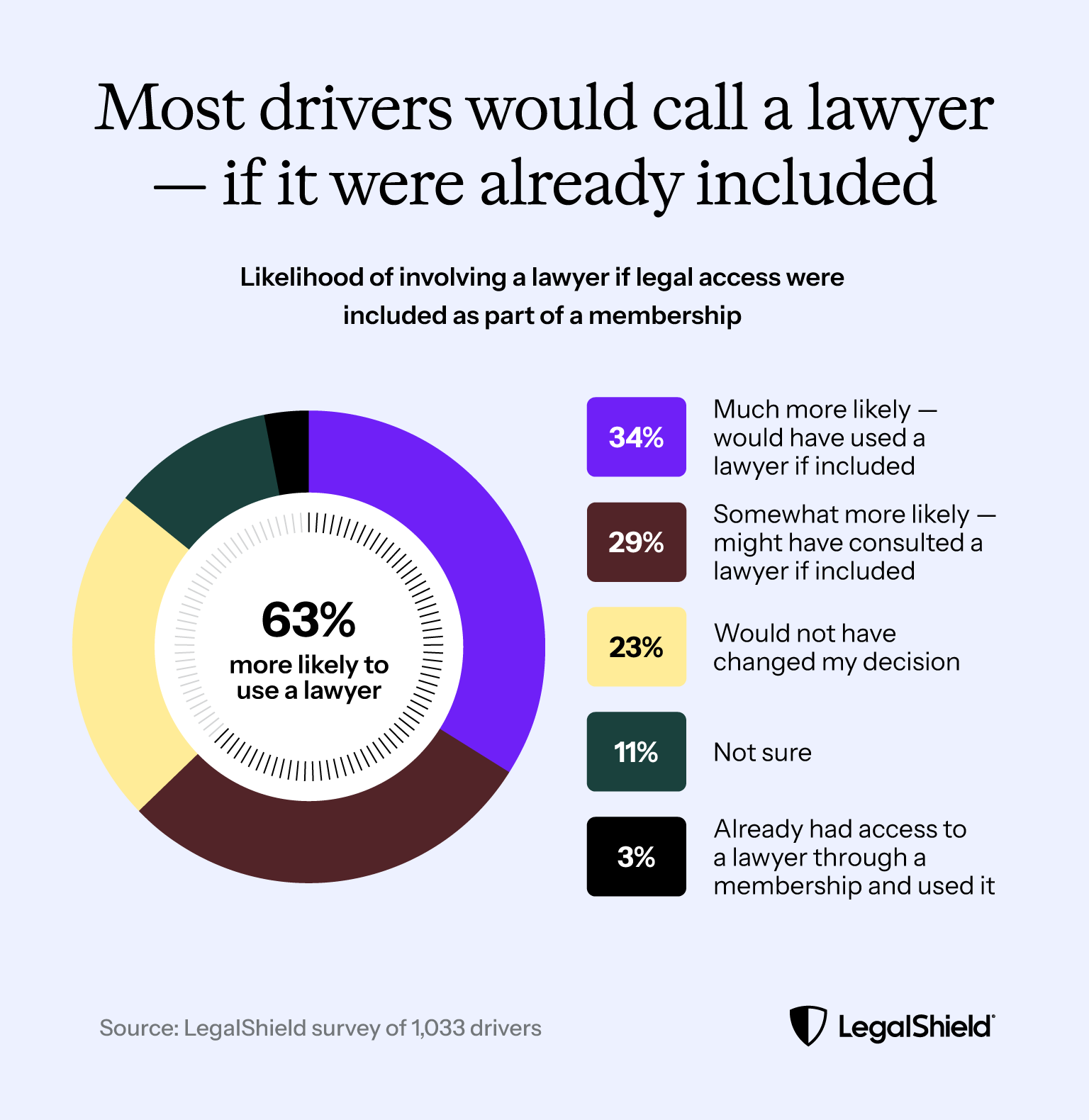

Looking back, more than half (53%) said legal guidance might have helped somewhere along the way. That tracks with what I hear. The regret, when it comes, is about the decisions made under time pressure without a full picture.

And when we asked whether having a lawyer already available through a membership would have changed their approach, 63% said yes. That’s nearly triple the number of people who actually got any legal help during their claim.

The assumption I run into most is that legal help means a retainer and a long process. For most claims, it's simpler than people expect and easier to use before you sign than after.

What a car accident really costs you, and how to be ready next time

Most people handle a claim alone because they want to move on. I understand that. An accident is stressful, and the last thing anyone wants is to extend it. But moving fast and being protected are different things. For a meaningful share of drivers, the cost of closing quickly didn't appear until later.

The pattern the data keeps confirming is how much of the financial fallout is preventable. Knowing you can ask question or take more time before signing is just being informed. And being informed before the moment arrives is almost always easier than trying to catch up after.

If you're reading this before an accident, that's the best position to be in. You can take your time to explore what options you may still have.

Methodology

The survey was conducted by LegalShield via Centiment. The survey was fielded between March 31 and April 1, 2026. The results are based on 1,033 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and had filed an auto insurance claim in the past three years. Data is unweighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

How to Sign as a Power of Attorney Agent to Represent a Loved One

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

•

6 min read

Author Name

,

Author Title

August 4, 2026

Personal Property

5 min read

How to Avoid Probate With Thoughtful Estate Planning

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.

•

5 min read

Author Name

,

Author Title

July 31, 2026

Personal Property

5 min read

Personal Representative vs. Executor: Who Does What?

An executor is always a type of personal representative, but a personal representative isn't always an executor. Learn about the differences and what each does.

•

5 min read

Author Name

,

Author Title

July 27, 2026

Personal Property

6 min read

How to Set Up a Living Trust: People and Considerations Involved

A Living Trust lets you decide now what happens to your home, savings, and other assets when you die.

•

6 min read

Author Name

,

Author Title

July 24, 2026

Personal Property

5 min read

How Funding a Trust Works, and Why It Matters

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

•

5 min read

Author Name

,

Author Title

July 23, 2026

Personal Property

3 min read

Fiduciary vs. Trustee: Which One Do You Actually Need?

Fiduciary and trustees are similar concepts, but have key differences. A Trustee is a type of fiduciary. Every Trustee is a fiduciary, but not every fiduciary is a Trustee.

•

3 min read

Author Name

,

Author Title

July 16, 2026

Personal Property

9 min read

What Does Et Al. Mean on a Deed? A Guide to Real Estate Terminology

Et al. on a deed means there are unnamed co-owners listed on your property title. Learn what it means and how to remove et al from deed paperwork.

•

9 min read

Author Name

,

Author Title

July 8, 2026

Personal Property

9 min read

Revocable vs. Irrevocable Trust: Which Is Right for You?

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

•

9 min read

Author Name

,

Author Title

July 2, 2026

Thank you! You're subscribed!

Oops! Something went wrong while submitting the form.