Personal Property

6 min read

Heirs vs. Beneficiaries: Who Inherits a Loved One's Estate?

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

A Revocable Trust keeps you in control but leaves your assets exposed to creditors, while an Irrevocable Trust protects your assets and reduces estate taxes by permanently transferring ownership out of your hands.

What if something happened to you tomorrow? Would your family have everything they need to carry out your wishes and settle your estate? It’s not pleasant to think about, but estate planning can be complicated. Wills must go through court probate, which can take a long time. Some people use Trusts to pass important assets down directly, which can potentially help your family sooner.

There are two general Trust structures. A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

We’re here to help break down how each Trust works, how they differ, and what to look for when choosing between them. Understanding the trade-offs is a great starting point, but we also recommend legal assistance with each step of the process. We’ll tell you how a LegalShield provider lawyer can help you with these big legal decisions!

Both Trust types help your family avoid probate, but they take very different approaches to control, taxes, and asset protection. Check out this table to see how they compare:

.png)

Think of a Revocable Trust like a suitcase. You pack it, you unpack it, you swap things in and out as your life changes. Formally, a Revocable Trust (also called a Living Trust or Revocable Living Trust) is a legal arrangement you create during your lifetime to hold and manage your assets. You still control everything.

In most cases, you serve as your own Trustee. You can add property, remove it, change your beneficiaries, or dissolve the Trust entirely. When you die, your successor Trustee steps in and distributes everything according to your instructions without a probate court involved.

What is a Revocable Trust good for? Mostly, it's a cleaner, faster, and more private way to pass assets to the people you love or organizations like charities. Because you still control the assets, you don’t have creditor protection and there is no separate tax return. But for families focused on avoiding probate and keeping things simple, it's often the right place to start.

A Revocable living Trust offers several practical advantages:

A Revocable Trust comes with some limitations:

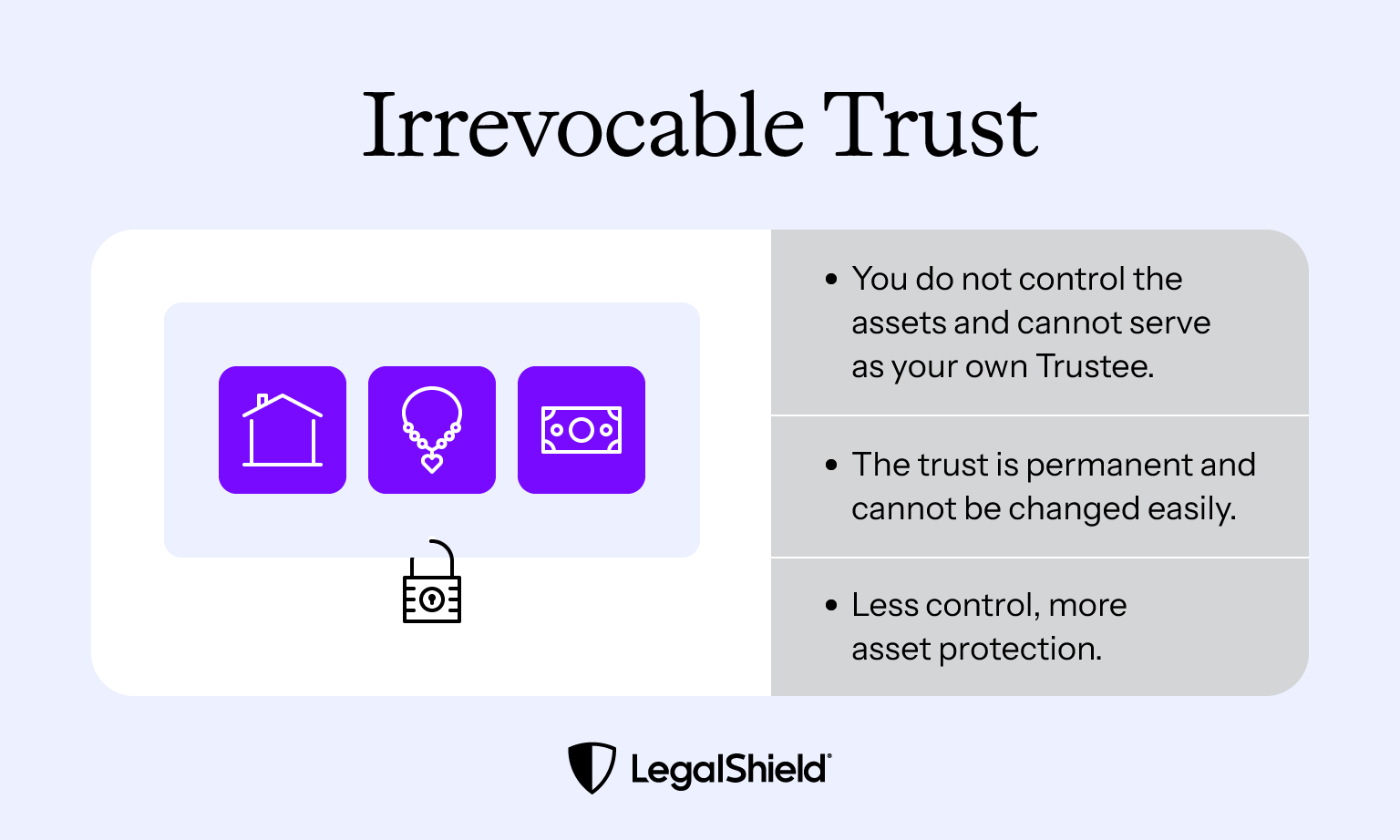

An Irrevocable Trust works very differently from a Revocable one. When you transfer assets into an Irrevocable Trust, you give up ownership. The assets no longer belong to you — they belong to the Trust. You can't take them back or change the terms without significant legal intervention. That might sound like a bad deal. For the right circumstances, it isn't.

When assets leave your legal ownership, two things tend to happen. Creditors can no longer easily reach them because they're no longer yours to claim. And those assets leave your taxable estate, which matters for families whose estates may exceed the federal estate tax exemption.

Because you give up control, you also give up the right to serve as your own Trustee. An independent Trustee manages the assets and follows the Trust's terms. The Trust gets its own tax ID number and files its own annual tax return as a separate legal entity.

Here are some benefits that come with transferring ownership to an Irrevocable Trust:

An Irrevocable Trust offers meaningful protection, but it also comes with real trade-offs:

These are the differences that matter most when making the Revocable vs. Irrevocable Trust decision.

With a Revocable Trust, you stay in charge. You serve as your own Trustee, manage the assets day-to-day, and can update the terms as your life changes. Whether it’s a new baby, a divorce, or you finally bought your dream lakehouse, the document evolves with you.

An Irrevocable Trust works differently. Because the whole point is legal separation between you and the assets, you generally can't serve as your own Trustee. A third party manages the assets according to the Trust's terms, and changes typically require either unanimous beneficiary consent or a court order.

One important transition: a Revocable Trust typically becomes Irrevocable upon the death of the surviving grantor. Your successor Trustee steps in, the terms lock, and distribution begins without probate. Understanding their rights as a Trust beneficiary helps clarify what that transition means for the people you leave behind.

Revocable Trusts are tax-neutral during your lifetime. The Trust uses your Social Security number, and income flows through to your personal tax return. The IRS essentially treats it as if it doesn't exist while you're alive.

An Irrevocable Trust is different. It files its own tax return under its own tax ID number, and income kept inside the Trust can be taxed at higher rates than it would be in your hands. Trust income quickly hits high taxation, so you should discuss this with an accountant.

Assets inside an Irrevocable Trust leave your taxable estate entirely. Transferring assets in is also typically treated as a completed gift, which may require filing a gift tax return. An estate tax planning overview can help you understand how these rules may apply.

A Revocable Trust generally doesn't protect assets against lawsuits or legal judgments. An Irrevocable Trust works differently. Once assets transfer in, you no longer have a legal claim to them, and neither do creditors in most cases. That separation is what provides the protection.

You have to run your Irrevocable Trust according to its terms and any state laws to maintain protection, or else a court could find your Trust invalid.

An example of using an Irrevocable Trust in asset protection is the business owner in a high-risk industry, like construction. A business owner can utilize an Irrevocable Trust to hold high value assets like retirement accounts to add another layer of protection against claims against their business and ultimately them personally.

The right choice for you depends on what you're trying to protect, how much control you want to keep, and where you are in life. The framework below isn't legal advice. It's a starting point for thinking through your priorities before you talk to a lawyer.

Some families use both, with a Revocable Trust for everyday assets and an Irrevocable Trust for high-value or liability-exposed assets. Your plan can grow with you. A solid estate planning guide can help you see how Trusts fit into the bigger picture before you speak with a lawyer.

Choosing the right Trust structure is one of the more consequential estate planning decisions you can make, and the details matter. That’s why LegalShield offers affordable plans to give you access to the legal advice you deserve. A LegalShield provider lawyer can help you understand which structure fits your situation.

Premium Plan members can also access basic Revocable Trust preparation through a provider law firm. Get estate planning guidance.

Sources:

1 Internal Revenue Service. (n.d.). What's new — estate and gift tax. https://www.irs.gov/businesses/small-businesses-self-employed/whats-new-estate-and-gift-tax

2 Internal Revenue Service. (2024, October 22). IRS releases tax inflation adjustments for tax year 2026, including amendments from the One Big Beautiful Bill (Rev. Proc. 2025-32). https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

3 Medicaid.gov. (n.d.). Eligibility policy — long-term services and supports look-back. https://www.medicaid.gov/medicaid/eligibility-policy

4 Internal Revenue Service. (n.d.). Frequently asked questions on gift taxes. https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes

5 Internal Revenue Service. (2026). Form 1041-ES — estimated income tax for estates and Trusts. https://www.irs.gov/pub/irs-access/f1041es_accessible.pdf

6 Cornell Law School Legal Information Institute. (n.d.). 26 U.S. Code § 2503 — Taxable gifts. https://www.law.cornell.edu/uscode/text/26/2503

Yes, a Revocable Trust typically becomes Irrevocable upon the surviving grantor's death. The successor Trustee steps in, the terms lock in place, and distribution begins according to your instructions. No court involvement or probate is required if the assets are properly titled. That automatic transition is one of the core reasons people set up Revocable Trusts in the first place.

In most cases, yes. A Trust usually only controls assets formally titled in its name, so a pour-over Will can catch anything left outside it and direct those assets into the Trust at death. Understanding living Trust costs involved in setting up both helps you plan ahead.

It depends on the type. A Revocable Trust typically costs a few hundred to a few thousand dollars in legal fees. An Irrevocable Trust generally costs more due to added complexity. DIY options exist, but errors in a Trust document can invalidate the arrangement or create tax consequences that cost far more to fix.

An Irrevocable Trust may help protect assets from long-term care expenses, but typically only if it's established well before you need care. Consulting with a lawyer about using an Irrevocable Trust for long-term health planning is a good first step.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

For many spouses, a postnup is simply about preventing confusion and making shared decisions before money questions get harder to discuss.

You might need your deed when you’re selling your home, adding a spouse to the deed, checking ownership, or trying to settle estate questions.

The difference between "per stirpes" and "per capita" can be confusing. They sound alike and both have to do with who inherits your assets if a named beneficiary dies. We'll explain the difference.

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.