Personal Property

6 min read

Planning for the future isn’t easy when it means thinking about what will happen after you’re gone. It often raises difficult questions about your assets, family, and legacy. Preparing a Living Trust is a step you can take to protect the people you love and ensure your wishes are carried out.

We assume that setting up a Living Trust is complicated or unaffordable. The reality is that the cost can vary depending on your needs, your state, and how you choose to create it.

In this guide, you will learn about the various types of Living Trusts, how much it costs to set one up, how it works, and what’s required to transfer your assets.

By the end of this post, you'll know which Living Trust offers the best protection for your assets and properties, and the cost to set up one without necessarily breaking the bank.

Not sure whether a trust is right for your situation? See how a living trust compares to a will before evaluating cost — the right choice depends on your assets, family situation, and goals.

A Living Trust is a legal document or entity that you can set up to protect your assets and transfer them to your beneficiaries after you’re gone. It helps make the process smoother for your family and potentially avoids probate.

As the grantor — the person who passes on their wealth or gives their loved ones an inheritance — you can set this up when you are alive by transferring your assets to the Trust. It will then “own” and “administer” those assets or properties.

This way, your assets will go to your beneficiaries according to your instructions after your death. Living Trusts also allow you — the person who established the Trust — to manage the assets or properties as a trustee. This means you can continue to add assets or remove them from the Trust as you see fit.

There are two main categories of Living Trusts. These are:

Choosing one depends on your goals. Let’s explore each of them.

A revocable Living Trust is a legal arrangement that allows you to add or remove assets from the trust, change beneficiaries, or update its terms as your life evolves.

The main benefit of a revocable Living Trust is its flexibility, which gives you control over your assets and lets you continually update the Trust as needed. This can be super helpful when your financial situation, family dynamics, or long-term plans change over time.

Its downside, however, is that because you maintain control over the trust, its assets are still considered part of your estate for tax purposes. The IRS can charge you taxes on these assets, while your creditors or lenders can get them to repay your debts.

On the other hand, once you set up an irrevocable Living Trust, you cannot modify or change anything, including your conditions or beneficiaries. So, it requires you to be sure of the “permanence” of the assets, properties, and/or beneficiaries. However, what an irrevocable Living Trust gives up in flexibility and control, it makes up for in asset protection and tax planning.

An irrevocable Living Trust is basically a separate legal entity from you with its own tax ID, which means that neither creditors nor the tax man can touch it if you set it up correctly. There are several types of irrevocable Living Trusts. Examples include an irrevocable life insurance trust, a Medicaid asset protection trust, a charitable trust, and a dynasty trust.

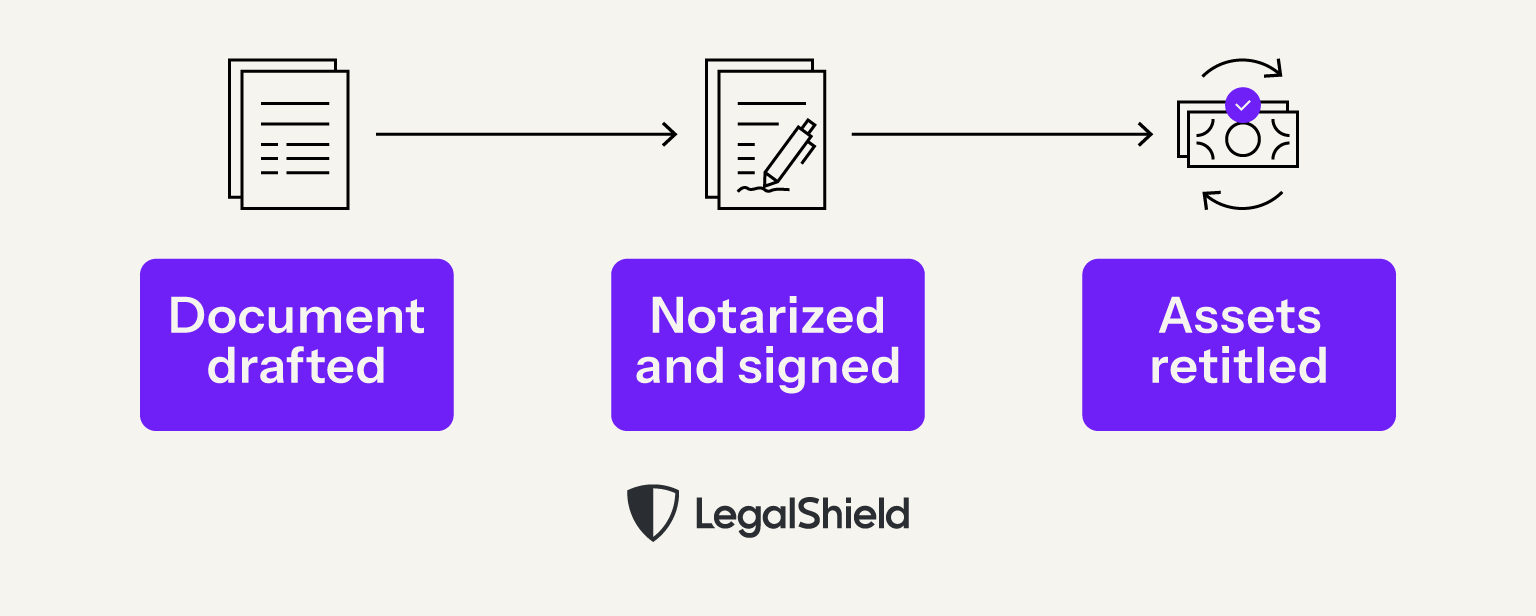

Understanding how a Living Trust works can help you decide whether you need one. Here’s a quick breakdown of the process:

The cost of a Living Trust can generally range from $400 to $5,000+. Your final fees will largely be based on factors like:

Another factor that can affect your Living Trust cost is its complexity. For instance, the price for setting up a separate or individual Living Trust varies from that of a joint or married trust.

A separate or individual Living Trust is best for keeping things simple, separating assets, and protecting all assets in the Trust. This is great for people with second marriages or children from previous relationships who want to keep certain assets or properties separate from their personal or joint assets.

A joint or married Living Trust works for couples with similar goals, is easy to set up, and allows the surviving spouse to assume responsibility for and manage it when one spouse passes on. This is great for couples who co-own properties — both names are on the title deed — assets, and finance.

Once funded, a living trust allows your heirs to transfer property to beneficiaries without going through probate — often saving months of court process and thousands in legal fees.

The only disadvantage is that, because it is not typically an independent or separate entity, there can be tax consequences, as well as increased risk if one party is sued or has creditors pursuing them. Whether you are creating a separate or joint Living Trust, there are three ways you can approach it, all of them with varying prices:

Online Living Trust services offer affordable, low-risk, and legally drafted solutions. While some legal service providers, such as LegalShield, offer Living Trust preparation as part of a broader legal plan membership.

For example, LegalShield’s Premium Plan includes preparation of a basic revocable Living Trust by an experienced lawyer in your state for a fixed fee.

Unlike DIY templates or online document services, this approach gives you access to a lawyer who can review your situation and prepare documents based on your needs. Because it’s part of a legal plan, costs are typically more affordable than what you would pay for standard legal services.

A Do-It-Yourself Living Trust typically costs between $50 and $1,000. These vary from DIY templates and kits that anyone can just create on their own to document generation services. These are for people with small estates or assets looking for affordable or low-cost living Trust options.

The most common problems with DIY Living Trusts include errors and inaccuracies when drafted, vague wording that can lead to family disagreements later, tax issues, and asset retitling problems. These can void the Trust or prevent your assets from being moved into the Trust.

Additionally, your estate may not bypass the probate process due to these mistakes, meaning your children or other beneficiaries may not receive the money and property you left to them on time. Only use this option if you are sure of what you’re doing.

The cost of Living Trust agreements drafted by lawyers tends to be higher than DIY or online services, with prices ranging from $1,500 to $5,000+, depending on the complexity of the estate, the value of assets, and state law compliance requirements.

But the biggest factor that influences pricing is the lawyer's hourly rates. If you have a large estate, special asset needs, multiple properties, blended families, sizable investments, and successful business interests, you may prefer this option, as it caters to your specific needs.

Although hiring a lawyer takes time and costs more, it could be a good option if you're looking for total asset protection, lower tax risk, and a bulletproof Living Trust.

Funding a trust involves changing the title on your assets — properties, investment accounts, retirement accounts, and business interests — from your name to the Trust’s name, designating beneficiaries, and moving the assets into the Trust.

This may involve creating a new title deed via a warranty or quitclaim deed for real estate, swapping bank account ownership details, or moving your business interests via an Assignment of Interest document, and naming beneficiaries or grantees. Maintenance costs are typically nonexistent if you’re the trustee.

However, maintenance fees may apply based on several factors, including:

Professionals typically charge certain fees to help draft, set up, or manage your Trust. Also, it costs more to manage multiple properties, business interests, and several beneficiaries with different needs in a Living Trust than it does to manage just one property and one beneficiary. State laws may also influence the fees associated with owning and maintaining a Living Trust.

Asset transfers to a Living Trust often come with fees. These include:

Additional costs may include professional trustee fees, which are usually a small percentage of the Trust’s asset value (typically between 0.5% and 2%), and filing or lawyer fees for business interest transfers.

A Living Trust doesn't have to cost you a small fortune. At LegalShield, we understand that not everyone can afford the high legal fees associated with setting up a trust. That's why we offer an affordable solution.

As mentioned earlier, LegalShield’s Premium Plan includes preparation of a basic revocable Living Trust by an experienced lawyer for a $250 fixed fee. While our other legal plans offer it at a discount from the provider law firm’s standard hourly rate.

With LegalShield’s estate planning and Living Trust costs, you can secure your loved ones’ futures and ensure that they get your assets without going through the lengthy and often expensive probate process. Let us help you set up your Living Trust today.

Not necessarily. It depends on whether you choose a DIY, an online service, or a lawyer-drafted Living Trust.

The first two can be cheaper than a Will. The last one, not so much. Regardless, it’s important to note that even if wills are cheaper, there may be long-term costs during probate, ultimately resulting in much higher fees overall.

Funding a Living Trust can be time-consuming and quite costly. Also, creditors may still be able to access your assets — same for anyone who files a lawsuit — and you may still have to pay taxes on it.

Also, certain asset classes, like retirement accounts, may not benefit from being in a trust. If in doubt, speak to an experienced estate planning lawyer about your options.

Yes, it is if the ultimate goal is to avoid the lengthy and expensive probate process and ensure the beneficiaries receive their inheritances on time after you pass on. The most significant benefit a living trust offers is probate avoidance — understanding when probate is required makes it clear why bypassing that process is worth the setup cost for most families.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

A partition action can help give you a path forward when you just can’t agree with a property co-owner — even if you’ve reached a stalemate.