Personal Property

6 min read

Heirs vs. Beneficiaries: Who Inherits a Loved One's Estate?

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

An irrevocable Trust is a legal arrangement that permanently transfers the ownership of certain assets from you into a Trust that you can’t easily change or revoke.

It’s normal to want to protect your assets, especially if you’re worried about the future. You might be thinking about how to plan for long-term care, protect your home, or make sure your family is secure. There are lots of legal tools to choose from. A Will is great, but an irrevocable Trust gives you more structure and protection.

An irrevocable Trust can help protect your assets from creditors and even lower some taxes. It also lets you decide who gets your assets when you pass away. Using an irrevocable Trust has both pros and cons. A LegalShield® provider lawyer can walk you through irrevocable Trusts and other estate planning options to help you decide which are right for you.

An irrevocable Trust is a legal structure that owns the assets you put into it. Once you transfer those assets, you usually can’t change the Trust terms without complicated legal steps.

Let’s give you some quick definitions of terms used with Trusts. The person who creates a Trust is the grantor. A trustee is a third-party who manages the Trust’s assets. Beneficiaries receive income or principal from the Trust.

Since there are quite a few important aspects of an irrevocable Trust, let’s check out some key features:

Once an irrevocable Trust owns your assets, the Trust is legally separate from you. In fact, the Trust becomes a separate taxpayer with its own Employer Identification Number (EIN). We’ll use an example to make how an irrevocable Trust works easier to understand.

Sarah has been saving for many years for retirement and has an account with a high net worth. She is concerned about lawsuits and wants to protect her large savings account from potential claims.

Revocable and irrevocable Trusts have different purposes. With a revocable Trust, you’ll keep flexibility and control during your lifetime. It’s a good way to organize your assets and help your heirs avoid probate.

Irrevocable Trusts focus on tax planning and long-term protection. You don’t have direct control of the assets after you transfer ownership to the Trust. Still, you should have some tax advantages and stronger protection against creditors. This type of Trust is often best for people who have a high net worth, need to protect their assets from creditors, or want to reduce estate taxes.

Irrevocable Trusts can help you in many ways:

Like most things, irrevocable Trusts come with some downsides. Some of the dangers of irrevocable Trusts include:

Irrevocable Trusts are generally more difficult to set up than revocable Trusts, and it’s best to get the help of a lawyer.

First, decide why you want to create the Trust. Not everyone does it for the same reason. Some people use irrevocable Trusts to protect assets.

Others are more interested in the tax benefits. Two types of irrevocable Trusts offer specific tax advantages:

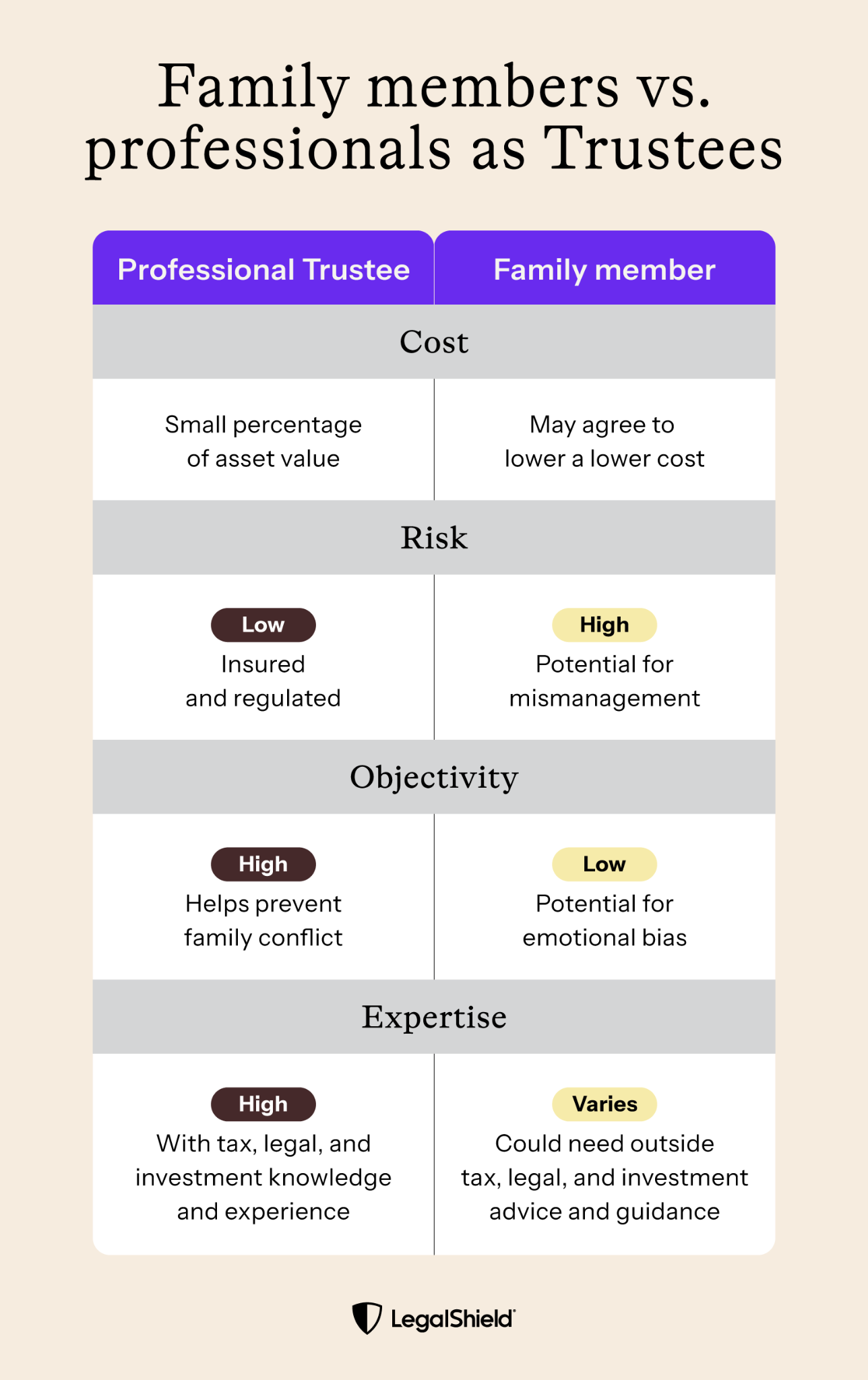

You’ll have to pick a trustee to oversee your Trust. That choice matters a lot because they’ll be in charge of everything. Mistakes can cause the Trust to lose value and lead to legal issues. Your goal is to choose a trustee who can manage the Trust responsibly.

You might want to select a family member. Choose someone who you believe is trustworthy and fiscally responsible. One benefit of selecting a family member is that they often won’t charge as much as a professional trustee. Weigh those benefits against their experience handling finances. Consider whether their emotional connection could cause family conflict.

Professional trustees may cost more, but they have experience. They know how to manage Trusts effectively and protect their irrevocable status with the IRS.

The type of assets you put into an irrevocable Trust matters. Let’s talk about the purpose for two main kinds of assets:

When you put growth assets, like real estate and stocks, into an irrevocable Trust, you’re freezing their value. Any appreciation in those assets can pass to beneficiaries tax-free. This type of asset transfer helps to avoid estate taxes, but it won’t generate fast cash flow. Be sure to talk to your financial advisor and CPA regarding the transfer of assets into an irrevocable Trust. Transfers of stock may require a sell-off, and the transfer of your residence may forfeit your homestead exemption.

You can also put liquid assets, like cash and liquid investments, into an irrevocable Trust. That transfer protects them immediately, and, those funds can help pay for taxes or Trust expenses.

Most people who create irrevocable Trusts do it for the protections they offer. But, those protections might not last if the Trust breaks rules. For example, the IRS looks closely at these Trusts. It wants to be sure that you’re not using the Trust for tax evasion. The IRS also looks at:

If you are involved in a lawsuit, the other party may try to prove that you transferred assets in order to protect them from the lawsuit, referred to as a “fraudulent conveyance”. Some states have lookback periods and other transfer restrictions.

Irrevocable Trust documents are complex. Even a small mistake in their preparation can lead to the IRS or a court not recognizing the Trust. This is too important to handle without the help of an experienced legal professional.

A LegalShield provider lawyer understands irrevocable Trusts and their advantages. With a LegalShield membership, your assigned provider law firm is in your state, so they also know state-specific laws that affect irrevocable Trusts. A DIY template can’t give you the safety net that personalized legal guidance can. A provider lawyer will help you make sure that you set your Trust up correctly.

Setting up an irrevocable Trust is only part of the process. The Trust doesn’t have an advantage until it has assets. You’ll need to title them using the Trust’s name and EIN.

The primary reason that Trusts fail isn’t because of bad drafting. It’s because grantors delay transferring their assets or don’t do it at all. Failing to fund your Trust leaves your assets vulnerable to the taxes and potential creditors you’re trying to avoid.

Understanding your estate planning goals is very important. An irrevocable Trust isn’t for everyone, but it might be right for you. You don’t have to figure it out on your own, though. Every situation is different, so legal support is invaluable.

Talk to a LegalShield provider lawyer who can answer your estate planning questions. They can give you guidance on the right Trust structure and make sure that your documents are legally sound. LegalShield members get reliable legal advice, with plans starting at around $1/day. Get help protecting your assets and heirs with LegalShield.

One of the key differences between an irrevocable Trust and a revocable Trust is that the grantor no longer has control of the assets, which is important for creditor protection. So adding yourself as a trustee defeats the purpose of an irrevocable Trust. Other options for a trustee are your spouse (as long as they are not also the grantor), a family member, professional trustee, or other responsible person.

Changing an irrevocable Trust is very hard to do. You can’t unless the court approves, the beneficiaries agree, and if you have a Trust Protector named in the Trust. Dissolving an irrevocable Trust is also legally complex, which includes defunding the Trust of assets.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

For many spouses, a postnup is simply about preventing confusion and making shared decisions before money questions get harder to discuss.

You might need your deed when you’re selling your home, adding a spouse to the deed, checking ownership, or trying to settle estate questions.

The difference between "per stirpes" and "per capita" can be confusing. They sound alike and both have to do with who inherits your assets if a named beneficiary dies. We'll explain the difference.

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.