A probate bond is basically an insurance policy that helps keep an estate’s executor or administrator accountable. It protects beneficiaries and creditors from financial loss caused by fraud, theft, or mismanagement.

When you're putting together an estate plan, one of the most important decisions you'll make is who you trust to carry it out. That person — your executor or administrator — will be responsible for managing your estate during probate, following state laws, and honoring the probate court's orders. A probate bond helps make sure they do.

If the executor or administrator makes a mistake or does something wrong intentionally, a probate bond is a financial safety net for your heirs and creditors. People may also call it an administrator bond, executor bond, fiduciary bond, estate bond, or surety bond. Whatever you call it, the goal stays the same: to protect the people who rely on the estate.

Let’s find out more about probate bonds:

Probate bond purpose

Protects the estate from financial harm caused by the executor's misconduct or mistakes

Who may need to get a bond

Court-appointed administrators or executors

Who pays for a probate bond

Usually paid by the estate, but the executor might have to pay upfront and request reimbursement

Who pays for claims

The bond pays first, but the executor has to repay that amount

Common necessary situations

The executor lives in a different state

Someone dies without a Will

The Will doesn't directly state that it waives the bond requirement

The beneficiaries or creditors request a probate bond

A beneficiary is a minor or incapacitated person

The probate court orders a bond

Understanding probate

When someone passes away, a probate court supervises the distribution of their estate. The court validates a Will or appoints an estate administrator if the person didn’t have a Will. The court oversees the process, but the executor or administrator handles the day-to-day responsibilities.

The probate process includes paying outstanding debts, such as medical bills, and giving the remaining assets to beneficiaries. It also allows ownership transfers of assets that belonged only to the deceased.

Not every asset has to go through probate. In fact, some parts of estate planning can help your heirs avoid probate:

Assets held in a living Trust

Life insurance and other accounts with named beneficiaries

Those designated as Payable or Transfer on Death

Property held in joint tenancy with right of survivorship

Depending on the size and complexity of your estate, the probate process can take months to over a year. And the details usually become public record.

How a probate bond works

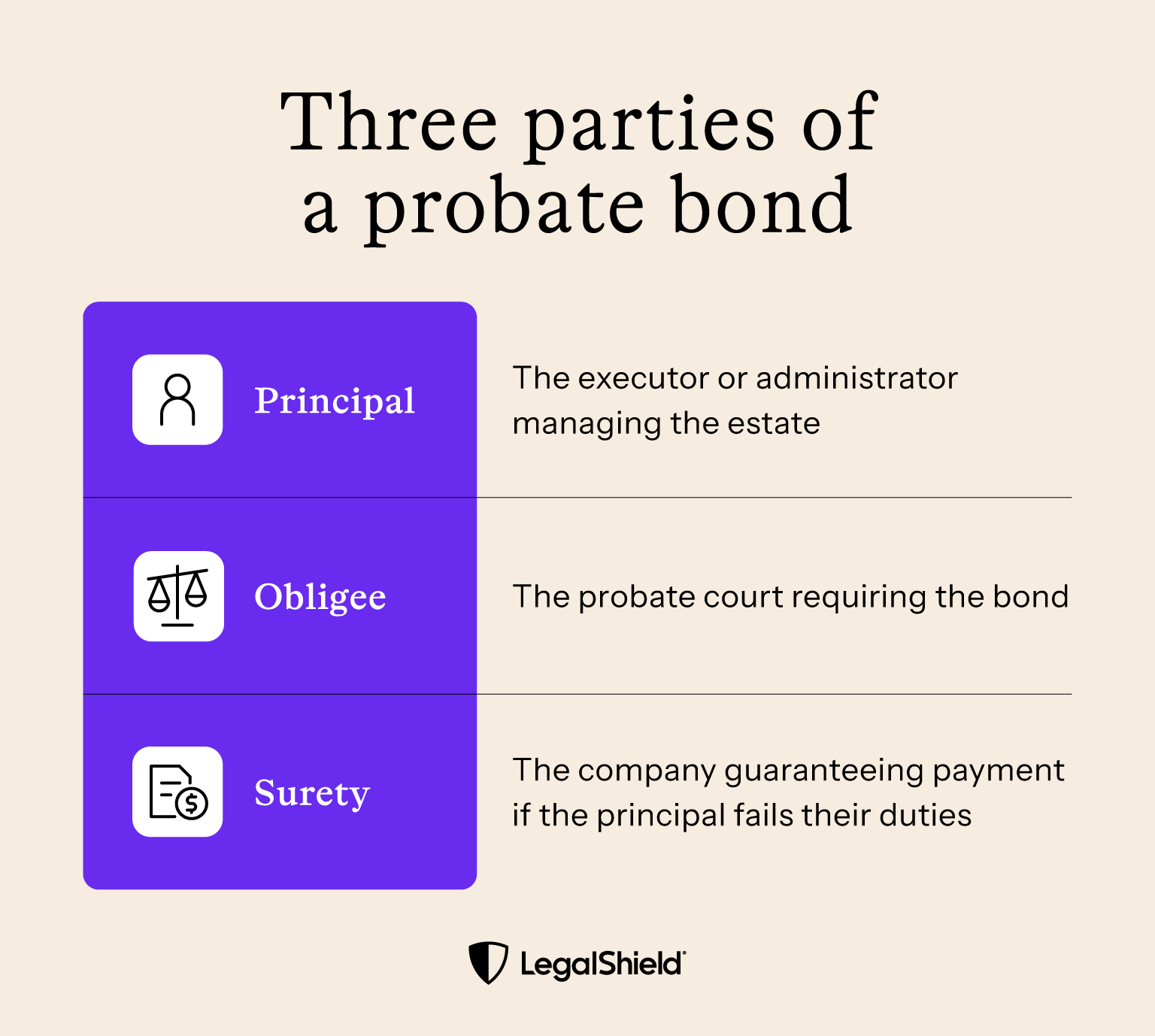

A probate bond is an agreement among three main parties:

Principal: The estate’s administrator (appointed by the court when there’s no Will) or executor (named in the Will to manage the estate)

Obligee: The probate court that requires the bond

Surety: The company that issues the bond and guarantees payment if needed

A probate bond creates accountability. The probate court expects the executor to follow the rules and manage the estate’s money honestly. If the executor doesn’t do this, someone can file a claim against the bond.

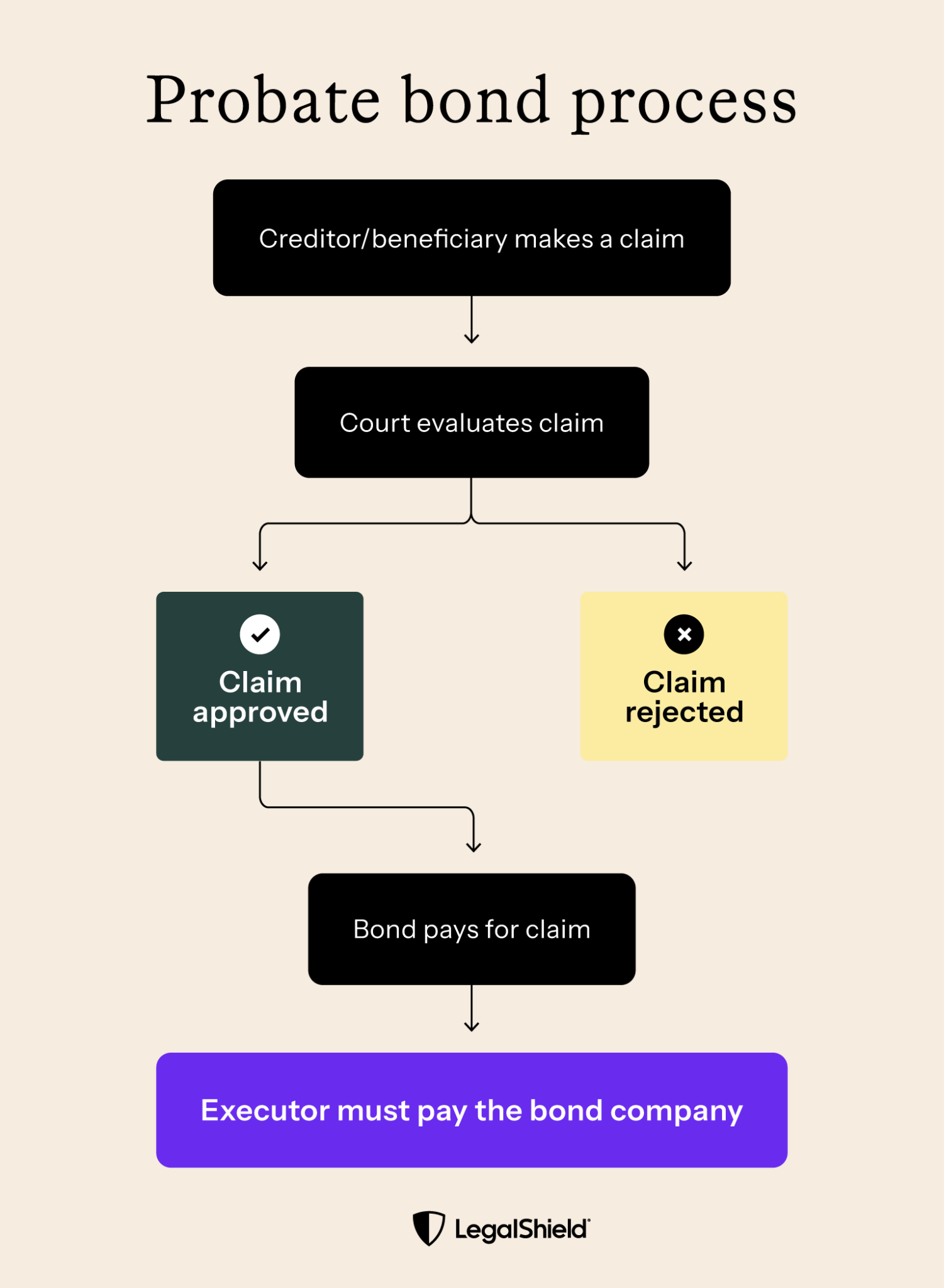

Here’s how the claims process works:

A creditor or beneficiary reports a problem to the probate court

The court reviews the claim and decides if the executor breached their duties

The surety company pays valid claims up to the bond amount

The executor has to pay the surety back for the full claim amount

The executor has a fiduciary duty to administer the estate in a way that follows the law and your wishes. A bond helps support that duty. The bond keeps beneficiaries and creditors from losing money if the executor does something wrong.

The executor is personally responsible for repaying the surety company if a claim is paid out. That's one reason a bond creates real accountability — the executor has personal financial skin in the game.

When a bond is needed

A probate bond is most commonly required because the Will calls for it, state law mandates it, or a beneficiary or creditor requests one. The probate court then confirms the requirement and determines the bond amount based on state laws, the estate's details, and the people involved. The court can also require a bond on its own if it has concerns about the executor or the circumstances of the estate.

Courts commonly require probate bonds in these types of situations:

The deceased died intestate (without a Will)

The executor lives in a different state

A beneficiary is a minor or an incapacitated person

Beneficiaries or creditors request a bond

There are conflicts among the beneficiaries

The Will doesn’t waive a bond

State laws require one

There are concerns about executor misconduct

Even if a Will states that a bond isn’t needed, the judge can overrule that waiver if there’s a good reason.

How to get a probate bond

If a probate bond is required, the person you've named as executor will need to go through an approval process with a surety company. Here's what that typically involves:

Be appointed by the court as the estate’s executor or administrator.

Contact a licensed surety company that handles probate bonds

Complete the bond application

Go through the underwriting review process

In case you’re wondering, underwriting is a process that looks at the risk of issuing you a probate bond. The surety company checks the executor’s credit score and the estimated estate value. They might also decide whether you’re able to handle estate finances. If the estate is complex, they might see the bond as a high risk.

How much a probate bond costs

A probate bond’s cost is called a premium. The premium for a well-qualified applicant is typically a small percentage of the bond amount, but it varies.

In most cases, the estate pays the bond premium. The executor or administrator might have to pay it upfront and file for reimbursement.

The probate court usually decides the amount of a probate bond based on how much the estate is worth. They may also consider expected income and other financial factors.

Probate bond denials

Remember that the executor or administrator has to repay claims against a probate bond. Surety companies don't want to lose money. If the applicant has poor credit, a history of legal issues, or financial instability, it could look like they might not repay a bond claim. The company might deny the application.

If a surety company doesn’t approve a bond application, there may be other options. An executor might be able to get a bond from a different company, but the costs may be higher. The probate court could appoint a different executor. Or, it could add a co-administrator with a better financial profile.

Probate bonds and estate planning

So, now you know that a probate bond may be required during probate. That gives you the chance for smarter planning. An executor’s low credit score could lead to a bond denial, and that might mean the court would appoint someone of their choosing.

You may want to choose an executor who has a strong financial profile. Or, you could select co-executors to allow someone with a lower credit score to still serve.

You can state in your Will that your executor doesn’t need a probate bond. However, in some cases, it may not be up to you. The probate court can require one anyway, based on the circumstances of your estate, your beneficiaries, or your executor after your passing.

Use your LegalShield plan to get advice from a lawyer

Estate planning and probate have lots of moving parts, but you don’t have to navigate them alone. With an affordable LegalShield Membership, you can ask a provider lawyer in your state about all of your estate planning needs. Get the experienced legal guidance you need to protect your loved ones.

Common questions about probate bonds

What happens if my executor has bad credit?

An executor might qualify for a probate bond with bad credit if an executor can find a surety company that works with higher-risk applicants. The premium might be higher, though. If your executor cannot get a bond, , the court could appoint someone else to manage the estate For this reason, it is good to choose the right person, and his or her successor, to serve as executor.

How long does a probate bond stay in place?

A probate bond is usually active during the whole probate process. That can last several months or over a year. When the court closes the estate and releases the executor, the probate bond ends.

Can the family decide to skip a probate bond?

Families might want to waive the requirement of a probate bond, but the probate court has the final say.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

How to Sign as a Power of Attorney Agent to Represent a Loved One

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

•

6 min read

Author Name

,

Author Title

August 4, 2026

Personal Property

5 min read

How to Avoid Probate With Thoughtful Estate Planning

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.

•

5 min read

Author Name

,

Author Title

July 31, 2026

Personal Property

5 min read

Personal Representative vs. Executor: Who Does What?

An executor is always a type of personal representative, but a personal representative isn't always an executor. Learn about the differences and what each does.

•

5 min read

Author Name

,

Author Title

July 27, 2026

Personal Property

6 min read

How to Set Up a Living Trust: People and Considerations Involved

A Living Trust lets you decide now what happens to your home, savings, and other assets when you die.

•

6 min read

Author Name

,

Author Title

July 24, 2026

Personal Property

5 min read

How Funding a Trust Works, and Why It Matters

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

•

5 min read

Author Name

,

Author Title

July 23, 2026

Personal Property

3 min read

Fiduciary vs. Trustee: Which One Do You Actually Need?

Fiduciary and trustees are similar concepts, but have key differences. A Trustee is a type of fiduciary. Every Trustee is a fiduciary, but not every fiduciary is a Trustee.

•

3 min read

Author Name

,

Author Title

July 16, 2026

Personal Property

9 min read

What Does Et Al. Mean on a Deed? A Guide to Real Estate Terminology

Et al. on a deed means there are unnamed co-owners listed on your property title. Learn what it means and how to remove et al from deed paperwork.

•

9 min read

Author Name

,

Author Title

July 8, 2026

Personal Property

9 min read

Revocable vs. Irrevocable Trust: Which Is Right for You?

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

•

9 min read

Author Name

,

Author Title

July 2, 2026

Thank you! You're subscribed!

Oops! Something went wrong while submitting the form.