A special warranty deed is a document that transfers ownership of property with limitations on the warranty. The seller guarantees the property's title is clear only during their time of ownership, not before.

Buying a home is a huge accomplishment. You've toured properties, made an offer, and finally reached closing day. Part of the process includes a warranty that protects you against undisclosed claims like liens on the property. So, you’re covered, right? Well, not necessarily, especially if you see a document called a "special warranty deed."

This document determines who is responsible if something goes wrong based on the property's past. And unlike other deeds, it leaves a gap in protection that many buyers don't see coming.

The deed controls what happens if a hidden lien, an ownership dispute, or a legal issue arises later. We’re here to help break it down in plain terms so you know exactly what you're agreeing to before you sign.

What is a special warranty deed?

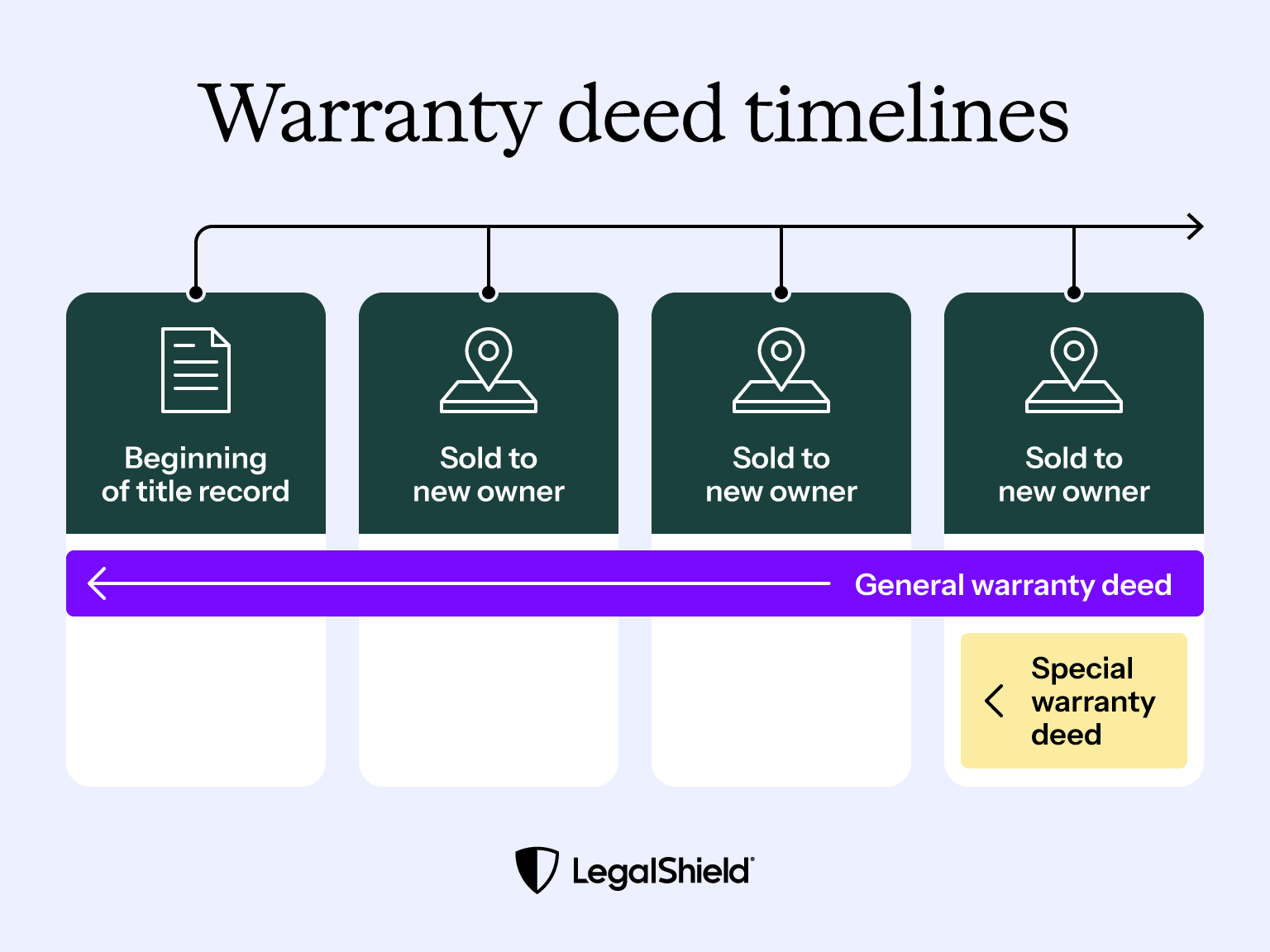

A seller who uses this deed guarantees only that the property's title was free of problems during the time they owned it. You may also see it called a limited warranty deed, and both terms refer to the same limited-coverage document.

Here's a simple way to think about it: Imagine buying a used car. The seller tells you, "I didn't damage it while I owned it." That may be true. But they aren't saying anything about the previous owners.

This deed works the same way. It sits between two other common options: a general warranty deed, which offers full protection, and a quitclaim deed, which offers almost none. Because of that, it is often called a "middle-ground" option.

You'll see it in situations where the seller lacks full knowledge of the property's history, like in commercial sales, foreclosures, and estate-related transactions. The name sounds strong, but the protection is limited.

How a special warranty deed works

With a special warranty deed, the seller makes two specific promises. First, they confirm that they legally own the property and have the right to sell it. Second, they confirm that they did not create any liens, debts, or legal claims against the property while they owned it. Those promises matter. However, they don’t often give the full picture.

The deed still transfers full ownership to you. You become the legal owner of the property. But you also take on the risk of past issues that the seller does not cover.

Old liens from previous owners

Unresolved legal claims

Errors in past title transfers

Easements that were not clearly disclosed

In other words, the deed gives you the property, but not complete peace of mind.

Special warranty deed vs. general warranty deed and quitclaim deed

To understand the risk, you need to compare this deed to the other common options. The comparison of these types of deeds below highlights the difference in protection.

A general warranty deed is considered the gold standard. It protects the buyer against title issues arising from the property's entire history. If a problem appears, the seller is responsible, even if the issue started decades ago.

A quitclaim deed offers the least protection. It transfers whatever interest the seller has, if any, without making any guarantees at all. Learn more about quitclaim deed basics. Sellers often prefer this deed type because it reduces their liability. This is especially true for banks, investors, and companies. They may not know the full history of the property, so they avoid taking responsibility for it.

Feature

General Warranty Deed

Special Warranty Deed

Quitclaim Deed

Protection level

High

Moderate

Low

Guarantee period

Full property history

Seller's ownership only

None

Seller liability

Covers all title defects

Only covers defects arising during the seller's ownership

No liability for any defects

Buyer risk

Low

Moderate

High

Common usage

Standard home sales

Foreclosures, commercial sales, estate sales

Family transfers

When you might encounter a special warranty deed

You are not likely to see every type of deed discussed in this article. The special warranty deed tends to show up in specific situations. These situations have one thing in common: the seller does not have full knowledge of the property's past.

We’ve laid out some common examples:

Foreclosed properties: Banks often sell homes they acquired through foreclosure. They were not the original owners, so they limit their responsibility.

Commercial real estate deals: Businesses aim to control risk. Using this deed helps them avoid long-term liability.

Estate sales: Executors may be selling property on behalf of someone who has passed away. They may not know the full title history. Understanding the timelines for property transfers after death matters in these situations.

New construction homes: Some builders use these deeds to limit exposure to past land issues.

In each case, the seller is setting a clear boundary. They are responsible for their time of ownership, and nothing before it. This is not necessarily a red flag, but it does mean you need to take extra steps to protect yourself, including understanding how transferring property to family members works if the transaction involves an estate or inheritance or obtaining a title search and opinion from a title company or lawyer.

Potential benefits and risks of special warranty deeds

The limited scope of special warranty deeds has advantages and drawbacks.

Benefits for sellers and buyers

There are a few reasons that sellers might use special warranty deeds, which you should understand as a buyer:

Exposure cap: The seller is not responsible for issues that occurred before they owned the property. This limits their risk and passes it on to you.

Non-occupants: Banks, investors, and companies can sell property without deep knowledge of its history.

For these reasons, you might see special warranty deeds as a red flag, but there are benefits for buyers, too, depending on the situation:

Access to high-value inventory: Many foreclosures and commercial properties use this deed structure.

Negotiation leverage: Buyers may be able to offer a lower purchase price due to increased risk.

Faster transactions: Fewer seller obligations can help speed up the closing process.

Risks to keep in mind

Careful review matters here. Without proper due diligence, a special warranty deed can expose buyers to unknown risks that turn into real financial problems.

These are some of the key concerns:

Inherited liens and encumbrances: Previous owners may have left unpaid debts tied to the property.

Competing ownership claims: Someone else could claim partial or full ownership based on past transactions.

Limited recourse against the seller: If the issue existed before their ownership, the seller is not responsible.

Easement disputes: You may discover access rights or restrictions that affect how you use the property.

Difficulties in resale or refinancing: Title issues can make it harder to sell the property or secure financing later.

Understanding the types of warranties in real estate documents can help you spot these issues before they become problems. A LegalShield® provider lawyer can also help you review the deed and flag anything that needs a closer look, which brings us to the next section.

LegalShield Personal Plans offer an affordable way to have a lawyer review your deed before you sign. The Advanced Plan is $49.95 per month and includes mortgage reviews and general document reviews. Instead of trying to interpret legal language on your own, you can get clear answers about what you are agreeing to.

We’ll connect you with a LegalShield Provider Law Firm that can help you identify red flags that are easy to miss. A provider lawyer can review the deed to make sure you understand what you're agreeing to before you sign.

Homes are life-changing purchases; professionals can help you move forward with confidence. Get real estate advice at each step of the process.

Common questions about special warranty deeds

Is a special warranty deed safe for a home buyer?

A special warranty deed can be safe for a home buyer, but it depends on what steps you take. Most buyers protect themselves by ordering a full title search and purchasing title insurance. These steps help uncover hidden issues and provide financial protection if something goes wrong. Without those safeguards, you are taking on more risk than you may realize.

Does a special warranty deed mean the title is clear?

No, this deed doesn't assure you that the title is clear. It only guarantees that the seller did not create title issues during their ownership. It does not confirm that the title was clear before they acquired the property. Problems from earlier owners can still exist.

Who usually pays for the title search?

Who pays for a title search is often negotiable. In many cases, the buyer pays for it because it protects their investment. Title insurance costs vary by state, but buyers typically pay a one-time fee ranging from $350 to $1,200, depending on the property and location.1 While it adds to your upfront costs, it can prevent much larger expenses later.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

How to Sign as a Power of Attorney Agent to Represent a Loved One

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

•

6 min read

Author Name

,

Author Title

August 4, 2026

Personal Property

5 min read

How to Avoid Probate With Thoughtful Estate Planning

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.

•

5 min read

Author Name

,

Author Title

July 31, 2026

Personal Property

5 min read

Personal Representative vs. Executor: Who Does What?

An executor is always a type of personal representative, but a personal representative isn't always an executor. Learn about the differences and what each does.

•

5 min read

Author Name

,

Author Title

July 27, 2026

Personal Property

6 min read

How to Set Up a Living Trust: People and Considerations Involved

A Living Trust lets you decide now what happens to your home, savings, and other assets when you die.

•

6 min read

Author Name

,

Author Title

July 24, 2026

Personal Property

5 min read

How Funding a Trust Works, and Why It Matters

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

•

5 min read

Author Name

,

Author Title

July 23, 2026

Personal Property

3 min read

Fiduciary vs. Trustee: Which One Do You Actually Need?

Fiduciary and trustees are similar concepts, but have key differences. A Trustee is a type of fiduciary. Every Trustee is a fiduciary, but not every fiduciary is a Trustee.

•

3 min read

Author Name

,

Author Title

July 16, 2026

Personal Property

9 min read

What Does Et Al. Mean on a Deed? A Guide to Real Estate Terminology

Et al. on a deed means there are unnamed co-owners listed on your property title. Learn what it means and how to remove et al from deed paperwork.

•

9 min read

Author Name

,

Author Title

July 8, 2026

Personal Property

9 min read

Revocable vs. Irrevocable Trust: Which Is Right for You?

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

•

9 min read

Author Name

,

Author Title

July 2, 2026

Thank you! You're subscribed!

Oops! Something went wrong while submitting the form.