Personal Property

6 min read

Heirs vs. Beneficiaries: Who Inherits a Loved One's Estate?

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

If you need inheritance money quickly, a probate loan allows you to borrow money using your inheritance as collateral. Probate loans are great, but come with several considerations:

Losing a loved one is hard enough, but having to go through a lengthy probate process to receive an inheritance can make an already difficult time more challenging. There might be bills that you can’t pay because the probate court is taking its time handling the deceased’s estate. Thankfully, there are probate loans that can help.

Probate loans offer a quick way to get cash using your inheritance as collateral for the money you’re borrowing. While they could be helpful, there are potential drawbacks to know about, which we discuss further in the following sections.

Probate loans offer quick access to cash at the cost of potentially high fees.

Below is a quick summary of how they work:

In addition to the probate loan, there’s also the probate advance (sometimes called an inheritance advance). Both exist to make it easier to obtain cash from an inheritance, but work in different ways. These differences are summarized in the following table.

There are three major differences to emphasize. First, probate loan lenders primarily earn their profit from interest. Probate advance lenders mostly earn their money from the advance fee.

Second, probate loans sometimes require monthly payments until the loan is fully repaid. Probate advances require a lump sum that the probate advance lender collects directly from the estate.

Third, with a probate loan, the lender’s primary legal interest is with the borrower. With a probate advance, the lender acquires a legal interest in the estate. Basically, the probate advance lender pays the advance to the heir. In return, the lender now has a legal right to a portion of the heir’s inheritance.

Probate loans can offer several useful benefits, but come with risks, which we summarize below.

Obtaining a probate loan can offer the following benefits:

As beneficial as a probate loan can be, there are risks to take into account before signing on any dotted line:

Not all financial obligations require a probate loan. However, below are some reasons why someone might need one.

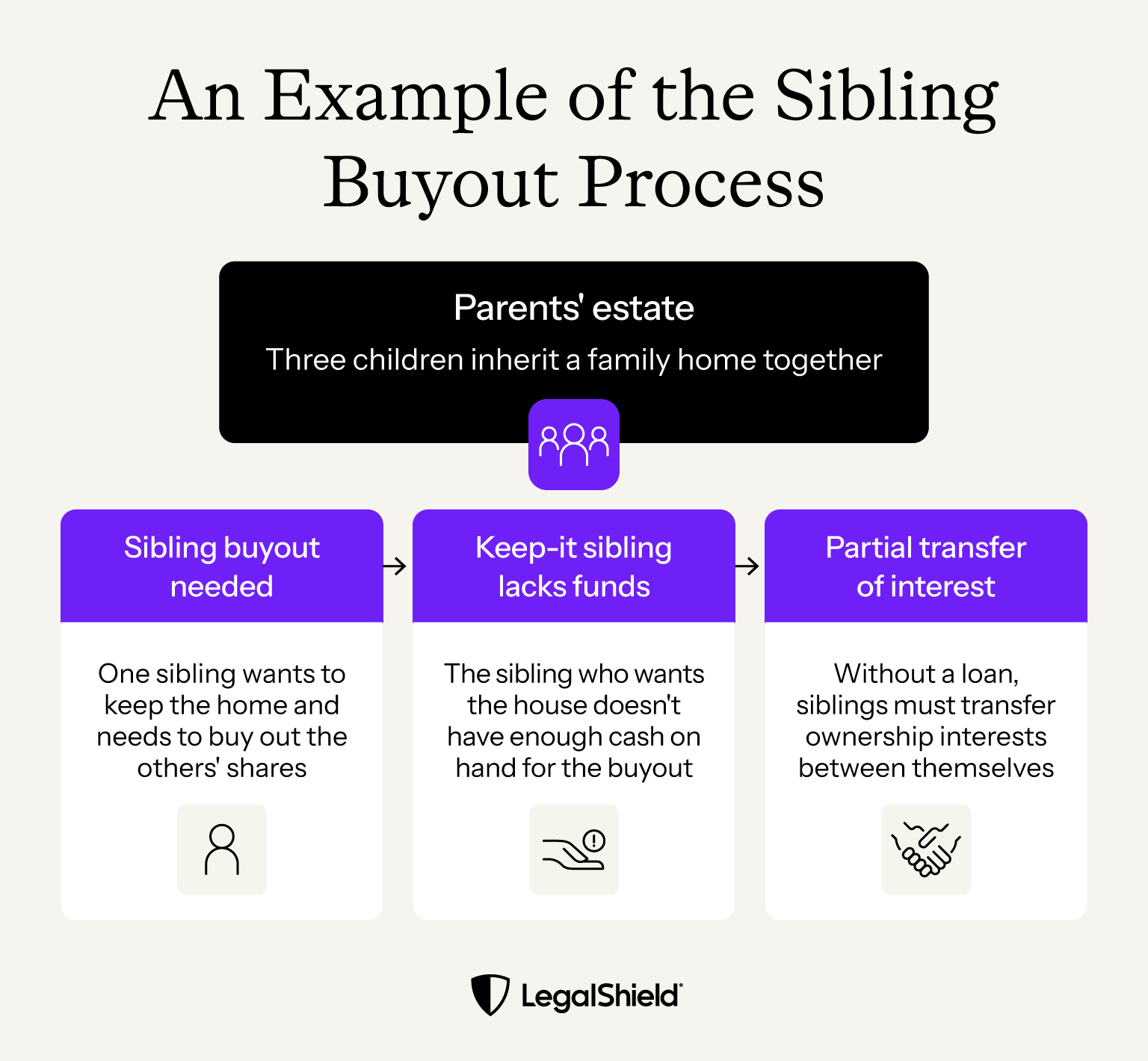

California’s Proposition 19 allows children to inherit their parents’ family home (or farm) without creating a new owner for property tax purposes. This is an important benefit because the value of a family home is often significantly higher at the time of the parents’ passing than when they first bought it.

If multiple children stand to inherit a single home, they may lose the benefits of Proposition 19. The transfer from the parents to the children can usually avoid a property tax reassessment. But when several of the children wish to sell their interest in the home to get their share of the home’s value, a property tax reassessment occurs.

To avoid this reassessment, one of the children can buy out their siblings’ interests in the home. This allows a direct transfer from the parents to a single child while providing the tax benefits from Proposition 19. But most individuals don’t have the cash needed to buy out multiple siblings. A probate loan can provide the cash for this purpose.

Heirs sometimes disagree on what to do with an inheritance. An heir can sometimes resolve these disagreements by buying out another heir. Probate loans can help if an heir lacks the cash to buy out the other heir.

Executors and heirs don’t usually need to use their personal funds to pay the debts and bills of the estate, such as funeral costs. Instead, the estate uses cash or property of the deceased to pay these costs. Estate funds also pay most of the other probate court costs, including probate lawyer fees and the probate bond.

Even though the estate is legally responsible for these bills, an executor or personal administrator may need to initially pay these costs out-of-pocket. The estate can then reimburse them later.

In cases where an heir wishes to sue the estate (they may not be sure if someone has a valid will), the person suing will need to use their personal funds to pay for their lawyer.

Getting a probate loan is much faster than the probate process. Despite this, it’s not instant and involves several steps. The exact time can vary, but potential borrowers should expect the entire process to take several weeks.

Probate loans are a great way to meet immediate financial needs after losing someone close. Yet they come with their share of risks and costs that may make other options more attractive.

If you’re not sure how to proceed during the probate process, you might benefit from one of LegalShield’s Personal Plans. For a customizable price, you’ll have access to a provider lawyer who can answer probate questions and any others you might have about creating your own estate plan or overseeing the probate process as an executor.

Executors and estate administrators can apply as an heir would. The main difference is that the lender doesn’t have to notify the executor of the loan.

It depends on the specific probate loan and the borrower's credit history. Most probate loan rates range from 7% to 15% per year. But some lenders charge interest rates based on the loan amount.

For example, the first $100,000 borrowed might have a 5% rate, while the next $100,000 would have a 4% rate. Then the next $300,000 might have a 3% interest rate, and any amounts over $500,000 might have a 2% interest rate. In these situations, the probate loan provider should offer a probate loan fee calculator to help you estimate what your fees will be.

LegalShield® is a trademark of Pre-Paid Legal Services, Inc. (“LegalShield”). LegalShield provides this blog as a public service and for general information only. The information made available in this blog is meant to provide general information and is not intended to provide legal advice, render an opinion, or provide a recommendation as to a specific matter. The blog post is not a substitute for competent legal counsel from a licensed professional lawyer in the state or province where your legal issues exist, and you should seek legal counsel for your specific legal matter. All information by authors is accepted in good faith. However, LegalShield makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of such information. The materials contained herein are not regularly updated and may not reflect the most current legal information. No person should either act or refrain from acting on the basis of anything contained on this website. Nothing on this blog is meant to, or does, create an attorney-client relationship with any reader or user. An attorney-client relationship may be formed only after the execution of an engagement letter with an attorney and after that attorney has confirmed that no conflicts of interest exist. Nothing on this website, or information contained or transmitted by this website, is intended to be an advertisement or solicitation. Information contained in the blog may be provided by authors who could be a third-party paid contributor. LegalShield provides access to legal services offered by a network of provider law firms to LegalShield members through membership-based participation. LegalShield is not a law firm, and its officers, employees or sales associates do not directly or indirectly provide legal services, representation, or advice.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

For many spouses, a postnup is simply about preventing confusion and making shared decisions before money questions get harder to discuss.

You might need your deed when you’re selling your home, adding a spouse to the deed, checking ownership, or trying to settle estate questions.

The difference between "per stirpes" and "per capita" can be confusing. They sound alike and both have to do with who inherits your assets if a named beneficiary dies. We'll explain the difference.

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.