Personal Property

6 min read

Thinking about what will happen to your home in the future isn’t always easy. For many, it starts with a simple goal: making things easier for the people they care about. Perhaps that’s why you’re looking into how to start a trust to hold important assets like your real estate. Real estate can include your home or, sometimes, empty land. Either way, transferring real estate to your trust is one of the most important steps in the estate planning process.

A trust can help your family avoid the time, cost, and stress of probate. And give you more control over how your home is handled later. Instead of going through court, your home can pass directly to the people you’ve chosen.

It’s not always easy to think about, but it can bring real peace of mind once it’s done. In this guide, we’ll walk you through how putting a house in a trust works, the steps to do it, and what to consider before you get started.

A trust is a legal tool that helps manage your property during your life and pass it on after you’ve gone. When you put your home in a trust, you’re setting clear instructions for how it should be handled and who should receive it.

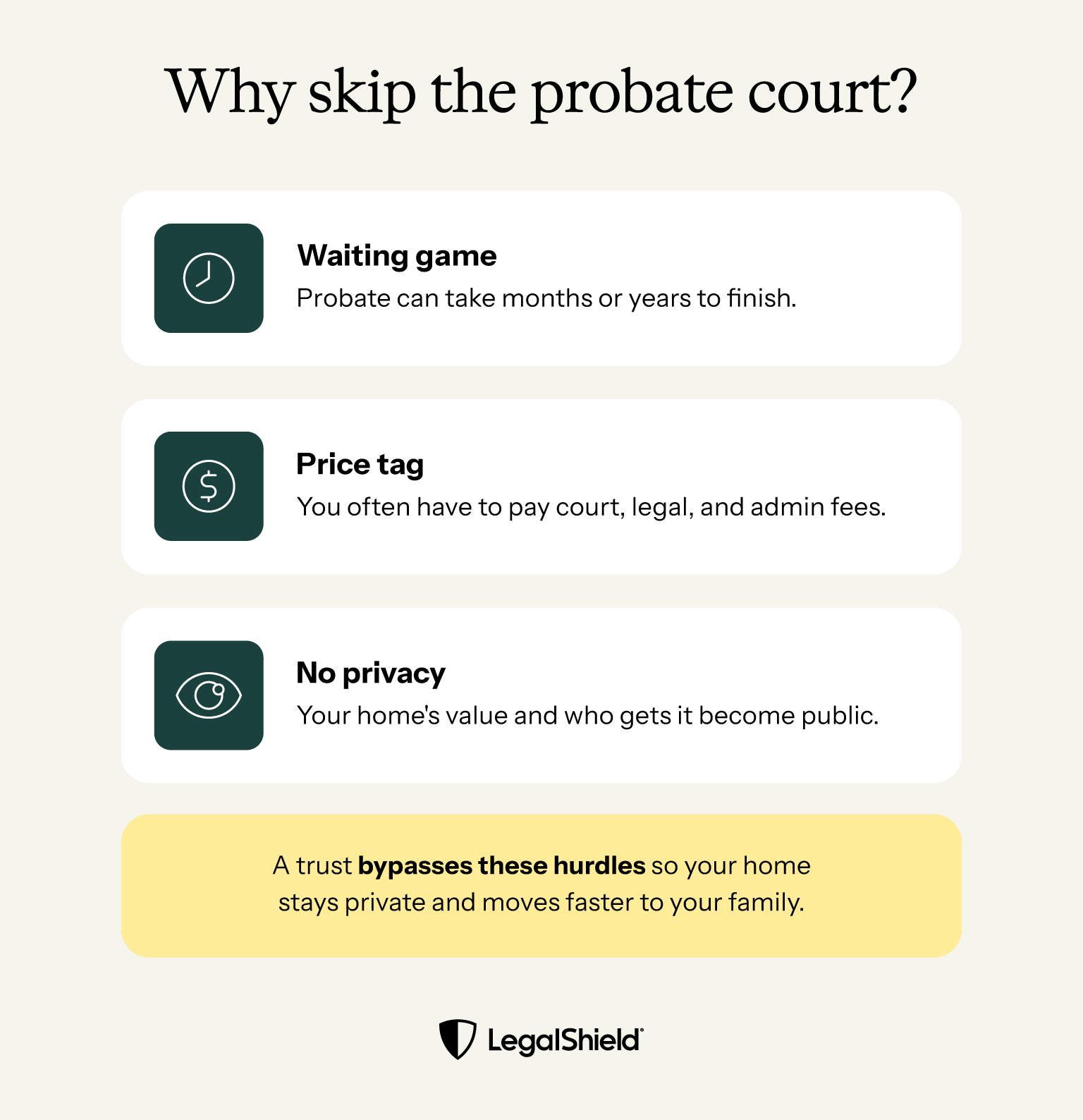

One of the biggest reasons is avoiding probate — the court process that distributes assets after someone dies. Probate can be:

Placing your home in a trust may help you avoid probate. That allows your property to pass more quickly and with fewer complications.

Privacy is a big pro here. Unlike a Will, which becomes part of the public record during probate, a trust typically stays private — meaning details about the home and who inherits it are not publicly available.

It also helps to understand the key people involved in a trust:

Putting your home into a trust takes more than just creating a document — you have to “fund” the trust by transferring ownership with a new deed recorded in the trust’s name.

Forming a trust and moving your home into it involves legal language that can vary by state. A lawyer can help ensure your documents are prepared correctly. This cuts the risk of errors, delays, and rejected filings.

If you’re looking for guidance without high hourly fees, LegalShield® Personal Plans give you access to a lawyer who can answer questions, review documents, and walk you through the process to help avoid common mistakes.

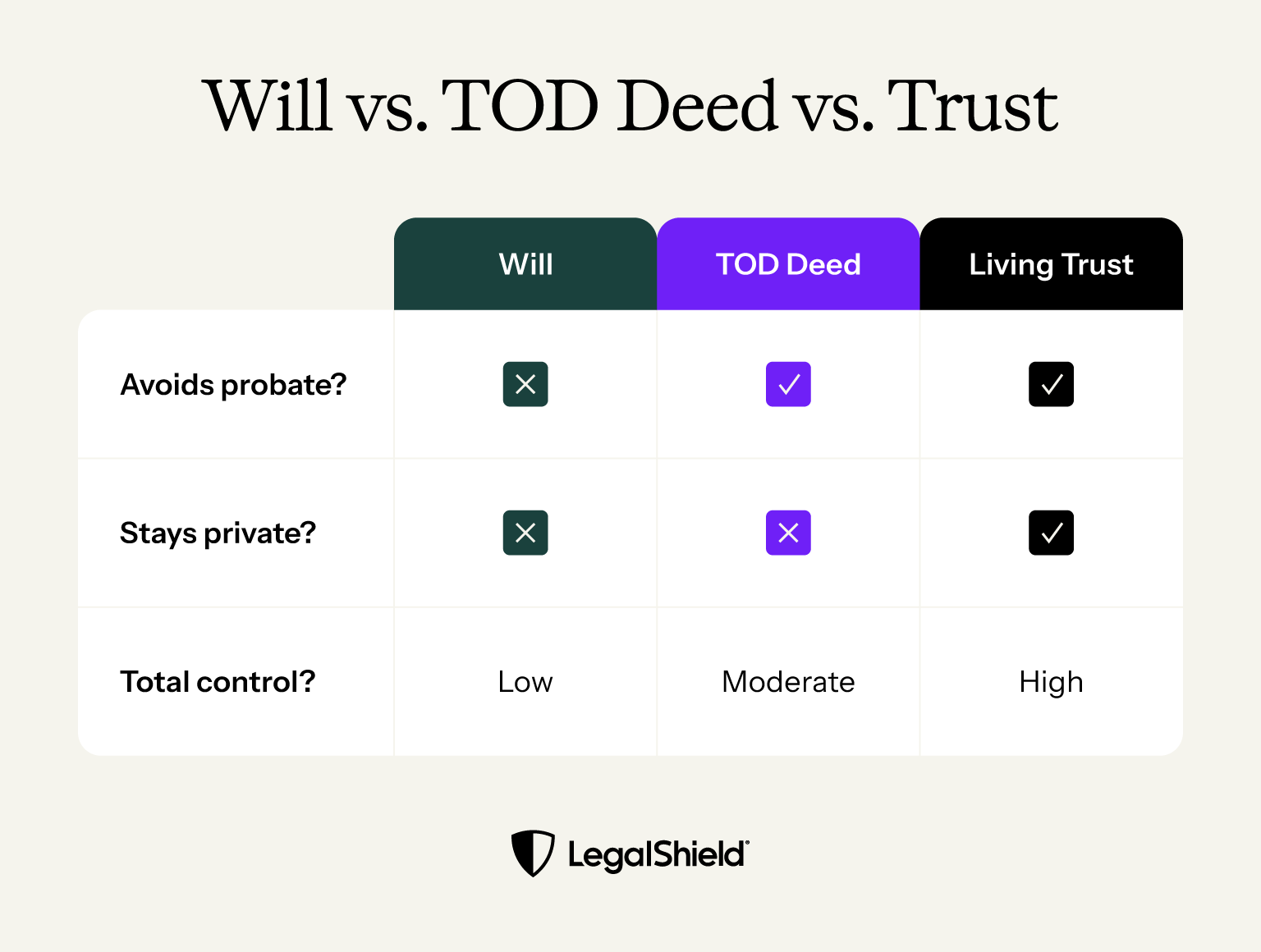

The first step is choosing the type of trust that fits your goals. For most homeowners, this means deciding between a revocable living trust or an irrevocable trust. Both can hold property. But they’re very different.

The most common estate planning option, a revocable living trust, lets you retain full control of your home and make changes to the trust at any time. An irrevocable trust is harder to modify and requires giving up direct control.

Here’s a simple comparison:

Once you’ve consulted with a lawyer on the type of trust you should choose, the next step is to have them create the document. This document explains how the trust works, who’s involved, and what will happen to your home. It’s the foundation of your plan. So it’s important to be clear and accurate from the start.

You’ll need to include details about the trust and the property it’ll hold. These can include:

You want your trust to work as intended and avoid confusion later. So, rely on a lawyer to handle the details for you.

The next step is to sign the trust to make it legally binding. In most states, this will mean signing the trust document in front of a notary. This person verifies your identity and confirms that you’re signing willingly. Your state might also require a witness at the signing.

Notarizing your trust helps make sure it’ll be recognized when it counts later. It may feel like a small step, but it’s an important one. Without proper signing and notarization, the trust may not hold up.

This is a key part of the process — often called the funding phase. For a trust to function as intended, your home typically needs to be transferred into it, which means preparing a new deed that moves ownership from your name to the trust’s name with the correct legal details.

Common deed options for this transfer include:

How you transfer your property to your trust can affect it in the future, so it is very important that you use the right deed form and that all of its contents are accurate. Mistakes can be costly when it is time to transfer a property to its next owner.

Once the deed is signed and notarized, file it with your county recorder’s office to update the public record. Be aware that there might be other forms to file along with your deed. A small recording fee usually applies, and once it’s recorded, the transfer is complete. The county recorder will often file a deed even if there are errors in the legal description or party information, so don’t rely on them to notify you of errors.

With the deed recorded, it’s time to update other documents tied to your home. Start with your homeowners’ insurance. The policy should list the trust as the owner now. You might also get the trust listed as another insured. This helps ensure there are no coverage gaps should you need to file a claim.

Also, let your mortgage lender know that you’ve transferred the property into a trust. A federal law, the Garn-St. Germain Depository Institutions Act of 1982 allows homeowners to transfer mortgaged residential property into a revocable living trust without triggering the mortgage’s “due-on-sale” clause. They may not necessarily change your account name and ownership, as it depends on the bank.

As a last step, review any other documents tied to your property. This might include property tax records or home equity lines of credit. Keeping everything consistent helps ensure that the trust is recognized as the owner of the home.

Federal law prevents lenders from enforcing a due-on-sale clause (a rule that requires full mortgage payoff if ownership changes) when you move a primary residence into a revocable living trust — as long as you remain the borrower and keep living in the home.

Your mortgage stays in place. You continue making payments under the same terms, including the interest rate and schedule.

Every mortgage is a little different, and yours might have language worth a second look before the transfer. With a LegalShield Personal Plan, you can connect with a provider law firm that will review your loan terms and answer questions about how the transfer fits with your specific situation.

Putting your home into a trust can offer real upside. But it also comes with a few trade-offs. Here’s a simple breakdown to help you weigh your options:

Benefits:

Drawbacks:

For many homeowners, the pros of putting their home into a trust outweigh the cons. That’s especially true when you think about avoiding probate and making things simpler for loved ones. But it’s important to understand both sides before you decide what’s right for your situation.

File name: probate-cons | Alt: Three reasons to skip probate with a trust: potentially long waits, fees, and the public listing of your home's value and who gets it.

There’s more than one way to pass your home to someone else. Some homeowners choose simpler options that need less setup. These alternatives can work well in some situations. But they usually offer less flexibility and control than a trust.

Some alternatives to using a trust include:

These options are simpler to set up. But they don’t offer you the same level of control as a trust. In most cases, ownership transfers directly to the named person without allowing you to set conditions or timing. You may also lose estate tax advantages. Other options, like leaving the home through a Will, may still require probate.

If you want more control, privacy, and long-term planning, a trust can be a strong option, especially when it’s set up with legal guidance.

Putting your house in a trust can help your family avoid probate, maintain privacy, and simplify how your home is handled in the future. And getting this trust set up the right way can make a meaningful difference for your loved ones.

With a LegalShield Personal Plan, you can connect with a provider lawyer who can answer your estate planning questions, review your documents, and help you feel confident that everything is set up the right way. Instead of navigating this process on your own, you’ll have guidance at each step.

Yes. You can still sell your house if it’s in a trust. If you’re using a revocable living trust, you typically stay in control of the property as the trustee. That means you can generally sell it similarly as if it were in your own name. You may have to provide a copy of your trust or certificate of trust when closing on the sale.

Living trust costs can vary. It depends on how you set up the trust and where you live. Some people use online tools to save on costs. Others work with a lawyer, which can cost several hundred to a few thousand dollars.

Transfer costs vary by state. You will also need to pay a small fee to record the new deed with your county. Many homeowners see these upfront costs as an investment in simplifying their family's lives later.

Many people still create a Will even if they have a trust. A Will can be a backup for any assets you didn’t transfer into the trust. This is sometimes called a pour-over Will. It directs remaining assets into the trust after your death. Having both documents can help you make sure you’ve left nothing out of your plan.

When you put your home in a revocable living trust, the trust becomes the legal owner. But you typically serve as the trustee and keep control over how you manage the property. So you can still live in the home, maintain it, and make decisions about it. The trust just holds the title on your behalf.

A trust has not fulfilled its purpose if it remains unfunded with your assets. If a lawyer helps you with your trust, they usually have additional services to help you fund your trust with your assets, like your real estate. If you prepare your trust on your own, you will need to arrange your own funding, whether you do so yourself or with a lawyer’s help. If you are not comfortable with the process of transferring your real estate to your trust, then you can get legal guidance to prepare the deed and explain how the process works in your state.

Communications Director at LegalShield overseeing content creation designed to make legal protection simple and approachable. He focuses on offering straightforward, trustworthy guidance that empowers people to make informed decisions about their legal rights and responsibilities.

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

A partition action can help give you a path forward when you just can’t agree with a property co-owner — even if you’ve reached a stalemate.