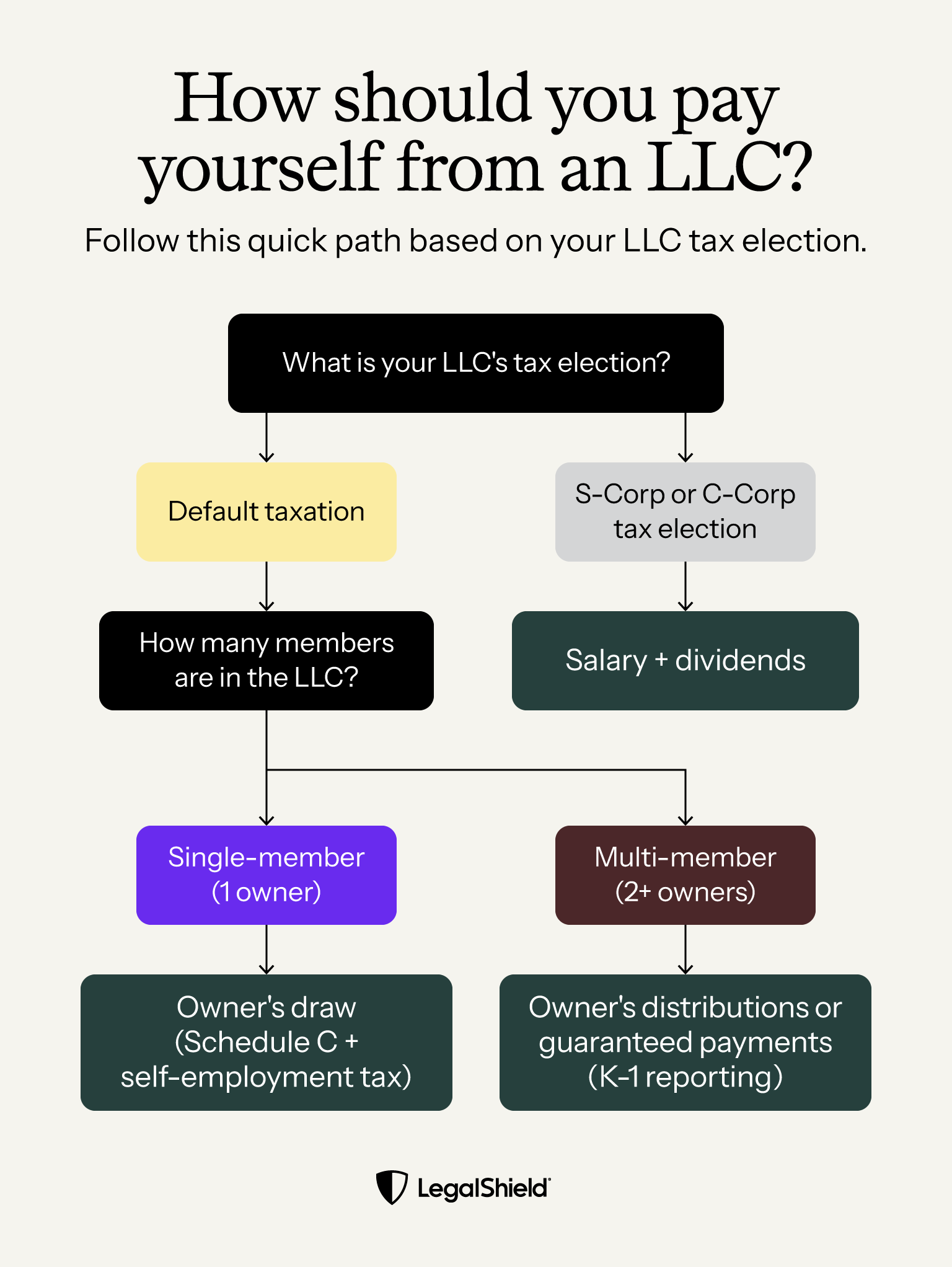

How you pay yourself depends on your LLC type and how it's taxed. There is no one-size-fits-all answer.

Single-member and multi-member LLCs use an owner's distribution by default to pay members.

LLCs taxed as S-Corps or C-Corps generally require owners to take a reasonable salary as a W-2 employee.

Your payment method determines how and when you pay taxes. Getting it wrong can mean a surprise bill at tax time.

No matter your structure, keep your business and personal finances separate.

Figuring out how to pay yourself from an LLC sounds simple until you realize your LLC type and tax classification determine everything. Take the wrong approach, and you could end up underpaying taxes all year and owing more at tax time in April. The right approach helps you manage your income and tax burden.

While this guide gives you useful information about paying yourself from an LLC, it is recommended that you consult with a CPA or an accountant so your LLC is set up with the best tax classification to meet your needs and maintain compliance with IRS regulations.

LLC Type

Payment Method

Default Tax Treatment

Who Pays the Tax

Single-member LLC

Owner's draw

Sole proprietorship (passthrough)

Owner pays self-employment tax on net profit

Multi-member LLC

Owner's distribution, guaranteed payments

Partnership (passthrough)

Each member pays self-employment tax on their share

LLC taxed as S-Corp

Salary + member distributions

S Corporation

Owner pays payroll tax on salary only; distributions don't incur self-employment tax

LLC taxed as C-Corp

Salary + member distributions

C Corporation

Company pays corporate tax on profits; individuals pay income tax on distributions

Four different ways to get paid from your LLC

Before you decide how to pay yourself from your LLC, look at your business structure and tax status. This will help guide your steps and make sure you're set up correctly before transferring any money. Here's a quick look at each payment method:

Owner's draw: This is a direct transfer of funds from your LLC's business account to your personal account. No taxes come out at the time of the transfer. You must make quarterly estimated payments for self-employment tax and income tax.

Guaranteed payments: Multi-member LLCs can pay members a regular salary. The company can deduct these salaries as a business expense, and members pay self-employment taxes.

Salary as an employee: When your LLC elects S-Corp or C-Corp tax treatment, you become a W-2 employee of your own company. Your LLC runs payroll, withholds taxes from each paycheck, and pays the employer portion of payroll taxes.

Member distributions: In addition to a normal salary, an LLC taxed as an S-Corp or C-Corp can distribute profits to owners as member distributions.

Owner payments like draws and distributions come from profits and don't have taxes withheld when you receive them. By contrast, a salary goes through payroll and has taxes withheld as you're paid.

Paying yourself from a single-member LLC

Payment method: Owner's draw

In a single-member LLC, business profits and losses flow directly to your personal tax return. You pay yourself through an owner's draw.

Taking a draw is simple, but it must be accurately reflected in your LLC’s books and records. Move funds from your LLC's business account to your personal account and record them in your bookkeeping as an owner's draw. Always keep this money separate from what your business needs to operate.

Your operating agreement might set rules for how much and how often your LLC can draw. Follow those rules to simplify your year-end reporting and protect yourself in the event of an audit.

Tax considerations

The IRS treats a single-member LLC as a "disregarded entity" by default. That's tax language, meaning the IRS does not recognize your LLC as separate from you for tax purposes.

Taking a draw doesn't lower your LLC's taxable income. You pay tax on your net profit, even if you don't take all of it out. For example, if your LLC makes $80,000 and you draw $50,000, you still owe tax on the full $80,000.

As a single-member LLC owner, you typically pay self-employment tax on your net earnings (currently at 15.3%, subject to applicable limits and changes). You report profits and losses on Schedule C with your personal Form 1040. You'll need to plan to make quarterly estimated tax payments. The IRS lets you deduct half of your self-employment tax from your gross income, which helps reduce the impact.

Paying yourself from a multi-member LLC

Payment method: Owner's distribution or guaranteed payments

In a multi-member LLC, each member can take an owner's distribution or receive guaranteed payments. Most members use distributions, taking money out as profits allow. Guaranteed payments work better for members who need a steady income, even when the LLC isn't making a profit.

Your LLC's documentation should set out the rules you create for distributions and guaranteed payments. That will make year-end reporting cleaner for everyone.

Tax considerations

A multi-member LLC is treated as a partnership by the IRS. Each member pays tax on their share of the LLC's profits, not just on what they actually withdrew during the year. That distinction catches many multi-member LLC owners off guard. Be sure you understand how it works before you set up your tax structure.

For example, if your LLC earns $100,000 and you own a 50% share, you owe self-employment tax on $50,000 even if you only drew $20,000 out of the business that year.

Multi-member LLCs file Form 1065, a partnership return, with the IRS each year. Each member receives a Schedule K-1 showing their individual share of income, deductions, and credits. Members report K-1 income on their personal returns and pay self-employment tax on their distributive share of income. Guaranteed payments are deductible by the LLC as a business expense and taxable to the receiving member as ordinary income.

Paying yourself from an LLC with an S-Corp election

Payment method: Salary + member distributions

When your LLC elects S-Corp status, you can become a W-2 employee of your business. Your LLC runs payroll and issues you a regular paycheck, just like any other employer. Setting a fair salary is one of the most important decisions you'll make when electing S-Corp status.

You can also take a dividend distribution from remaining profits in addition to your salary.

Tax considerations

As a W-2 employee, your LLC withholds federal and state income taxes, as well as Social Security and Medicare taxes, from each paycheck. Your LLC also pays the employer portion of Social Security and Medicare taxes.

One potential tax advantage comes from what happens to profits beyond your salary. Distributions to S-Corp members aren’t subject to self-employment tax. So if your LLC earns $150,000 and you pay yourself an $80,000 salary, you pay self-employment tax on $80,000 rather than the full $150,000. For a profitable LLC, that difference can be meaningful depending on your situation.

The IRS requires that your salary reflect what you would pay someone else to do your job. Paying yourself too little to maximize distributions may increase the likelihood of an audit trigger. Review your S-Corp and LLC options with a lawyer or CPA early in the process to avoid mistakes that can be hard to correct later.

Paying yourself from an LLC with a C-Corp election

Payment method: Salary + member distributions

As with an S-Corp, a C-Corp means you pay yourself a salary as a W-2 employee and withhold taxes from each paycheck. Many small LLC owners choose other structures over a C-Corp, depending on their goals. A C-Corp is often used by businesses that expect to reinvest earnings, raise outside money, or go public in the future.

Beyond a salary, you can distribute remaining profits to members as distributions. One benefit of the C-Corp structure is that your salary is deductible by the LLC as a business expense. Taking a reasonable salary reduces the LLC’s profits. That reduces the corporate tax bill before you consider member distributions.

Tax considerations

LLCs taxed as C-Corps are taxed at a flat 21% federal rate plus any applicable state income tax before any distributions are paid to members. When distributions are made, members also pay personal income tax on what they receive.

Avoiding double taxation

Double taxation means the company pays corporate tax on its profits, and then you also pay personal income tax when those profits come to you as dividends. There may be strategies that businesses consider to manage their total tax exposure.

Paying yourself a fair salary directly lowers the company's taxable profit, since salaries are deductible. Putting money into a retirement plan or paying for health insurance through the company also helps. Both are business expenses that decrease taxable income before the corporate tax rate applies.

Some owners choose to pay dividends in years when their personal income and tax rate are lower. Others keep profits in the company as retained earnings, delaying personal taxes until they take a distribution later. Each option has tradeoffs, so it's smart to work with your legal and tax advisors.

How to pay yourself and report via owner’s draw

To pay yourself via owner's draw, transfer money from your LLC's business account to your personal account. Since taxes aren't taken out automatically, you'll need to handle them yourself. Here's a general process to follow:

Step 1: Keep a separate business bank account

Open a dedicated business checking account if you haven't already. If you’re still in the early stages of setting up your LLC, go to your bank or credit union, bring your EIN and LLC formation documents, and set up an account in your LLC's name. It’s recommended to keep business and personal funds separate. Separate accounts make it easier to track earnings, expenses, and draws, and protect your limited liability status.

Step 2: Decide how much to draw

Check your cash flow after covering all business expenses and setting aside money for taxes. Only take out what the business can afford, not just what you want personally. Also, the LLC operating agreement usually sets rules about when and how much you can take in distributions.

Transfer the funds and label the transaction

Record the transfer in your bookkeeping software as an owner's distribution, not a business expense. Distributions don't reduce your LLC's taxable income.

Step 4: Pay quarterly estimated taxes

No taxes are automatically deducted from your draws. You pay the IRS directly on April 15, June 15, and September 15, with a final payment due January 15 of the following year, using Form 1040-ES. Small business owners just getting started should build these payments into their cash flow plan from day one.

Step 5: Report your income at year-end

Single-member LLC owners report profits on Schedule C with Form 1040. Multi-member LLC owners get a Schedule K-1 and report their share of income on their personal return. You report your net profit, not just the amount you drew out.

How to pay yourself and report via salary

If your LLC is taxed as an S-Corp or C-Corp, you pay yourself a salary through payroll. Taxes are taken out of each paycheck automatically, just like any other job.

Step 1: Figure out a reasonable salary

Look up what people in your role and industry typically earn. The IRS wants your salary to be consistent with fair market pay. Paying yourself too little to avoid payroll taxes can lead to an audit.

Step 2: Set up payroll

Most small business owners use a payroll service to make things easier and avoid mistakes. You can run payroll yourself, but the paperwork can pile up fast.

Step 3: Run payroll on a regular schedule

Pick a pay schedule and stick to it, whether weekly, biweekly, or monthly.

Step 4: File Form 941 each quarter

Form 941 reports the payroll taxes your LLC withheld and the employer contributions it paid. This filing is due every quarter.

Step 5: Issue yourself a W-2 at year-end

Your LLC gives you a W-2 just like any other employee. If you also received member distributions, they will appear on a Schedule K-1. Keeping good payroll records from the start makes things much easier as your business grows.

Get help with ongoing business management from LegalShield

Understanding how to pay yourself from your LLC is key, but the legal questions don't end there. As your business grows, you'll face ongoing questions about contracts, employment issues, and commercial disputes. LegalShield Business Plans give you access to a provider law firm in your state for a low monthly fee. You can speak with a provider lawyer who can help you understand your options, avoid common mistakes, and make more informed decisions as your business grows.

Your plan includes legal consultation on business legal matters, professional letters and calls made on your behalf, review of business-related documents, and collection letters to help you recover unpaid invoices. If a situation falls outside your plan's standard coverage, the provider law firm can still assist you with the discounted rate service.

Below, find answers to frequently asked questions about how to pay yourself from an LLC.

Can the owner of an LLC pay themselves through payroll?

Yes, an LLC owner can pay themselves through payroll, but only if the LLC has elected S-Corp or C-Corp tax treatment. In that situation, you must pay yourself a salary as a W-2 employee, with regular tax withholding and quarterly Form 941 filings.

Can I pay myself as a 1099 from my LLC?

Generally, no. In most cases, LLC owners pay themselves as a W-2 employee.

If your LLC pays you a salary through an S-Corp or C-Corp election, you receive a W-2 at year-end. If you take draws or distributions, you'll report that income on Schedule C or through your Schedule K-1.

Can I take money out of my LLC without paying taxes?

No, taking money out of your LLC without paying taxes isn't possible, even through an owner's draw or distribution. These do not trigger taxes at the moment of transfer, but you still owe self-employment tax and income tax on your share of the LLC's net profit. In a multi-member LLC, you owe tax on your share of profits whether or not you received a distribution.

What happens if my LLC makes no money?

If your LLC doesn't make money, you can still take a draw, but you pull from your own capital contributions rather than from profit. If there's no profit, you may not owe self-employment taxes for that period (depending on your situation), and you may qualify to deduct a business loss on your personal return.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

Trade Name: Definition, Examples, and How to Register a DBA

If you want to do business under a name that isn't your own legal name or your LLC's registered name, you need a trade name, also known as a doing business as (DBA) name.

•

6 min read

Author Name

,

Author Title

July 28, 2026

Small Business

5 min read

How To Create a Consulting Agreement for Your Business

A consulting agreement is a contract between a service provider, such as an independent contractor, and a recipient.

•

5 min read

Author Name

,

Author Title

July 28, 2026

Small Business

6 min read

What Is a Hold Harmless Agreement, and Do You Need One?

Hold harmless agreements can help reduce a business's liability by having signatories accept a certain amount of risk.

•

6 min read

Author Name

,

Author Title

July 9, 2026

Small Business

4 min read

How To Set Up an LLC in New York (and Why It's Unique)

Getting an LLC in New York generally involves choosing a business name, filing Articles of Organization with the New York Department of State, creating a written Operating Agreement, completing New York’s publication requirement, and handling tax and business setup steps, like getting an EIN.

•

4 min read

Author Name

,

Author Title

July 15, 2026

Small Business

5 min read

How To Franchise Your Business: A Six-Step Overview

Knowing how to franchise your business takes more than enthusiasm. It takes documented systems, legal preparation, and the right partners.

•

5 min read

Author Name

,

Author Title

June 17, 2026

Small Business

6 min read

How to Transfer Property to an LLC: A 5-Step Guide

In this guide, we walk you through how to transfer property to an LLC in just a few steps, along with key things to watch for so you can make this change with clarity and confidence.

•

6 min read

Author Name

,

Author Title

June 15, 2026

Small Business

9 min read

How To Create an Anonymous LLC: A Step-by-Step Guide to Business Privacy

It’s not available in every state, but certain jurisdictions allow you to form an LLC without listing members or managers in publicly searchable records.

•

9 min read

Author Name

,

Author Title

June 15, 2026

Small Business

5 min read

A Guide to Starting an LLC for Real Estate

We’ll talk about how to start an LLC for real estate, and go over some concerns about personal liability in case something goes wrong.

•

5 min read

Author Name

,

Author Title

June 12, 2026

Thank you! You're subscribed!

Oops! Something went wrong while submitting the form.