Personal Property

6 min read

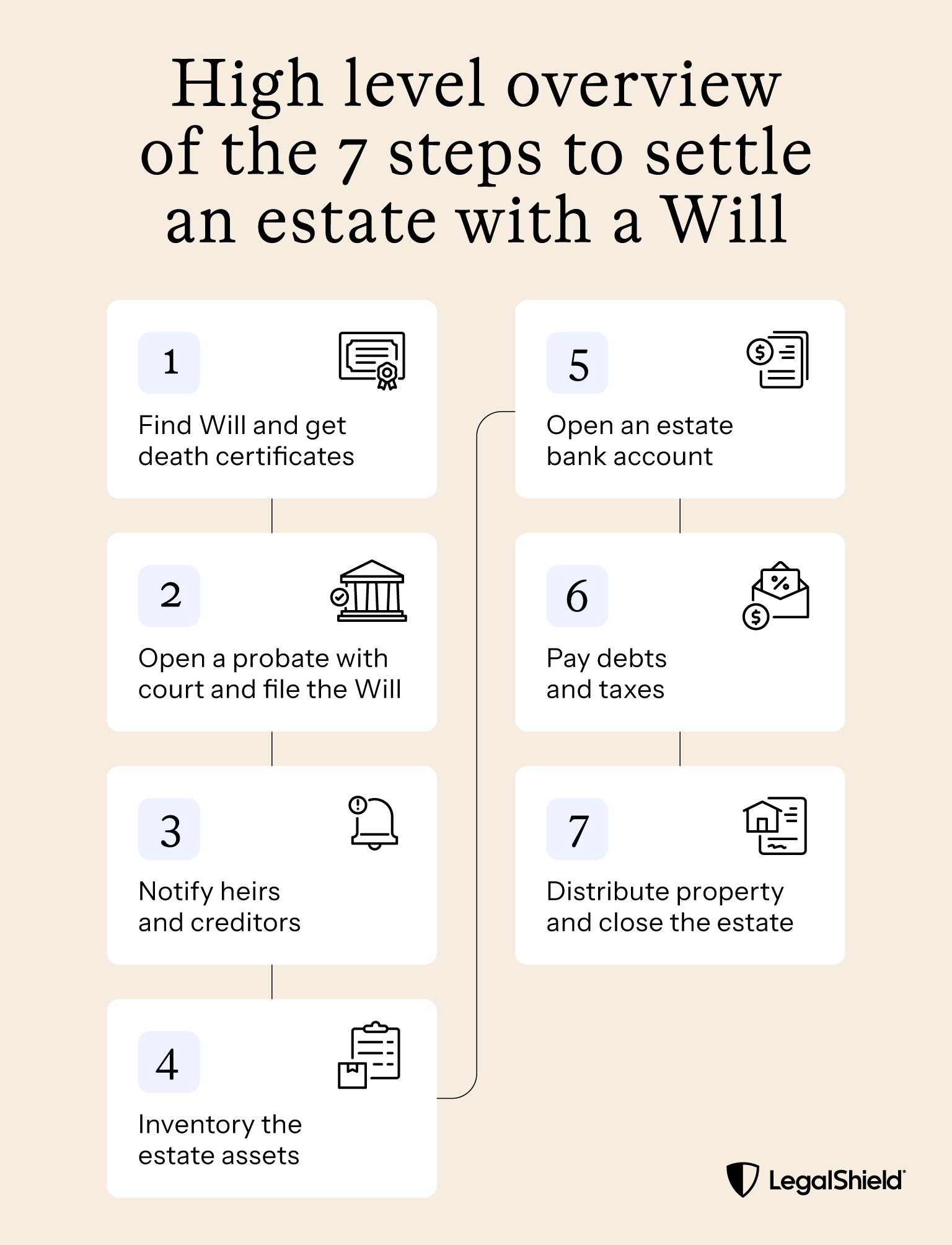

Settling an estate with a Will involves paying a deceased person's legal debts and distributing their assets according to their instructions. A Will makes the process clearer, but most estates still require court supervision to complete.

Losing someone is hard enough without also having to deal with legal paperwork. An executor is the person responsible for managing the estate of the deceased. They collect assets and pay debts and taxes. A Will sets out who's in charge and who gets which assets.

Estate settlement involves managing a deceased person's finances. As the executor, you'll pay their legal debts and distribute their assets to the people they named. The process often follows a general path. The seven steps below walk you through the general process for settling an estate with a Will. It’s important to follow the probate court’s directions and the advice of a lawyer.

Here's a checklist of documentation you need:

A Will guides the process, but it doesn't avoid probate court. Understanding when probate is required helps you plan the timeline. You'll need to open a probate case and file the original Will in the county where the deceased lived. The court will confirm the Will and appoint you as executor.

It can feel like a lot of administrative responsibility at once. Thankfully, the process is more straightforward than it first appears.

Once the court appoints you, it issues a document called Letters Testamentary. This serves as your official proof of authority. Banks, government agencies, title companies, and insurance providers may require these, so order several certified copies.

As executor, you're legally required to notify everyone with a stake in the estate. That means all estate beneficiaries named in the Will and all legal heirs — even those who won't receive anything. Heirs who aren't named still have the right to contest the Will for a defined period, so this step is typically required.

You've probably seen the dramatic "reading of the Will" scene in movies, featuring the lawyer, the wood-paneled office, and the gasping relatives.In reality, there is usually no formal ‘reading of the Will’. The executor or lawyer simply sends copies to all beneficiaries and heirs for them to review on their own.

Most states also require you to notify creditors. You'll send notices to the ones you know about. You'll also publish a formal notice in a local newspaper to notify unknown creditors. Anyone who wants to make a claim must do so within a set time limit.

Your job as executor is to track down and document everything the deceased owned at the time of death. It’s not uncommon for additional assets to be identified during this step. Sometimes a coin collection turns up tucked away in a closet. Sometimes you might discover a storage unit no one mentioned.

Higher-value items — real estate, collectibles, and business interests — require a professional appraisal. That provides a fair market value for tax purposes.

Here are some examples of what to include in your inventory:

As executor, you must manage estate funds carefully and always in the estate’s and beneficiaries' best interests. A dedicated estate bank account keeps everything separate and transparent.

Before you can open the account, you'll likely need an Employer Identification Number (EIN) for the estate. You can apply for one directly for free on the IRS website. It is recommended that you review the IRS instructions on filing for an estate EIN, and you should consult a CPA or lawyer if you have questions.

See our full guide on setting up an estate account for what to expect at the bank.

Before distributions are made to beneficiaries, the estate is generally responsible for paying debts and obligations. The good news is that you're not personally responsible for the deceased's debts. However, if there is a lot of debt to pay, the beneficiaries might not receive as much as they expect (or anything at all), so it’s a good idea to talk to beneficiaries about the financial realities early.

The estate may also carry tax obligations. You'll need to file the deceased's final personal income tax return covering the year in which they died. If the estate earns income during the settlement period, you may also need to file a separate estate income tax return using Form 1041. Understanding estate tax obligations is essential to protecting yourself and the beneficiaries.

Pay debts in this order:

After the court approves payment of expenses and debts, distribute the remaining assets in accordance with the Will and court approval. How long does it take to settle an estate? Timelines can vary depending on complexity or disputed estates.

Different asset types transfer in different ways. Here are some examples:

Closing the estate is the final step. You'll file a final accounting with the court. You'll give a copy to every beneficiary. The accounting sets out:

In most cases, once the court approves the accounting, you file a petition for discharge. The court issues an order formally closing the estate and releasing you from your duties.

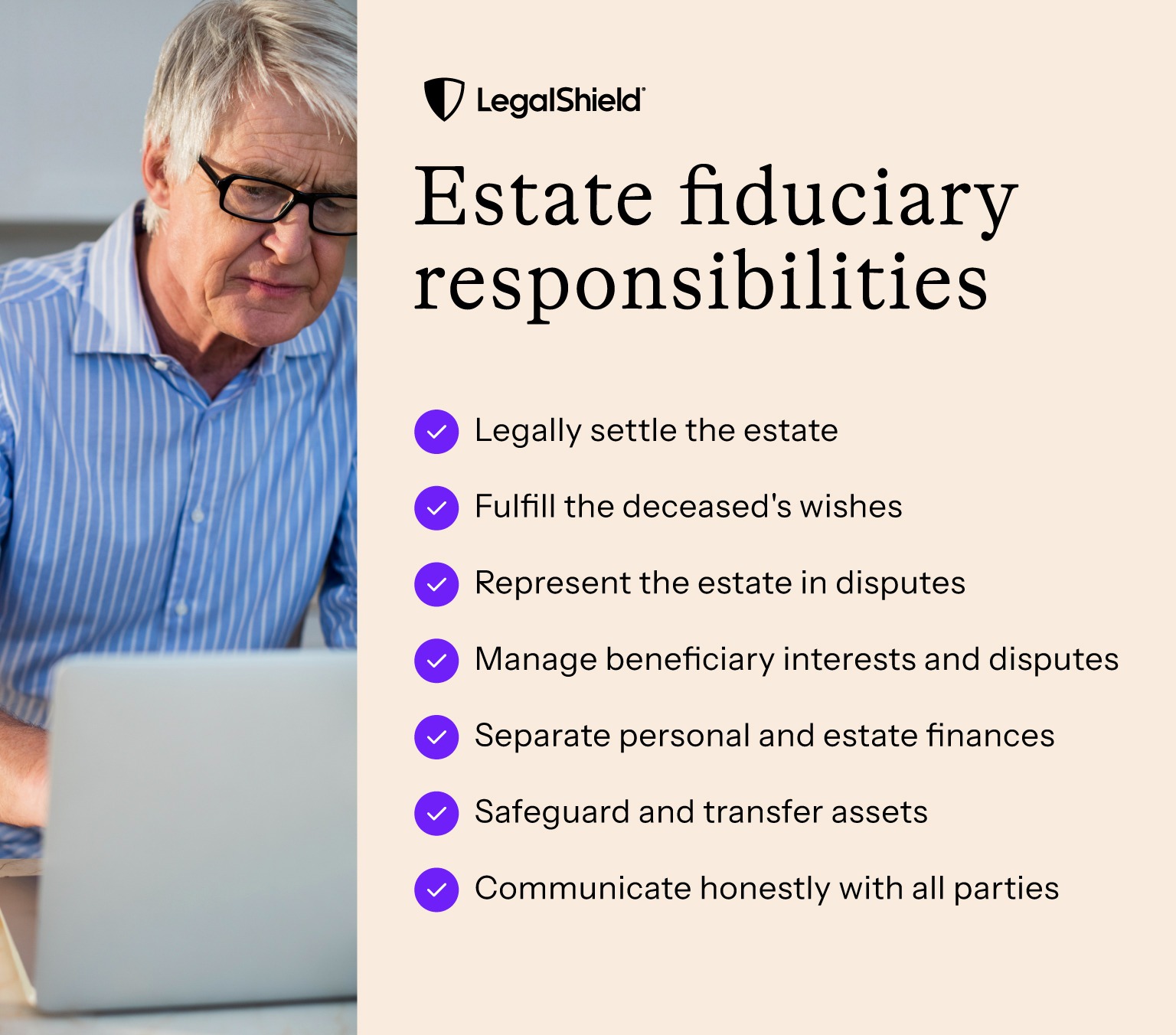

Settling an estate involves more than following a checklist. When you understand the key legal concepts, you can better avoid costly mistakes. That will help you protect yourself and the beneficiaries.

Having a fiduciary duty means you must set your personal interests aside, and you have a duty to settle the estate according to both the law and the wishes laid out in the Will.

This duty can become complicated if:

Due to the complexities of serving as an executor, it’s a good idea to speak to a lawyer to understand your responsibilities.

Title: fiduciary-duty | Alt text: An image listing some of the responsibilities of executors.

The probate court isn't always directly involved in the transfer of property. Some of the things that pass outside of probate include:

These non-probate assets don't appear in the estate inventory and don't affect the estate's closing timeline. This is the main area where estate planning documents and beneficiary designations control the settlement process.

Working with a lawyer throughout this process is worth serious consideration. An executor who makes even honest mistakes can face personal liability. A lawyer can advise you on your obligations, help you interpret the Will, and flag issues before they become disputes.

If you have to open a probate, a lawyer will be able to prepare the required filings and help navigate the required time frames and actions.

Acting as an executor comes with important legal responsibilities. You'll need to know how to settle an estate with a Will correctly at each step. Mistakes may create complications, including delays or disputes. Getting legal guidance early makes the process smoother for everyone involved.

With a LegalShield membership, you can access a provider lawyer for legal guidance without the uncertainty of hourly fees. You can also request a provider lawyer to review your Will before you finalize it.

Get estate planning guidance today.

Here are some questions people often ask about knowing how to settle an estate with a Will.

While most states don’t require a lawyer, many executors choose to seek legal guidance to better understand their responsibilities, avoid potential issues, and represent them in court. A legal consultation will help you understand your duties and avoid mistakes that can lead to personal liability.

Almost every estate goes through some form of probate, regardless of size. Simplified procedures exist for smaller estates when there isn’t a Will, but thresholds vary by state. Even a modest estate with real estate in the deceased's name alone typically requires probate. Check your state's specific rules with a lawyer before assuming simplified procedures apply.

Beneficiaries generally don't pay income tax on assets they inherit. The executor files the deceased's final personal income tax return covering income through the date of death. The federal estate tax applies only to very large estates. Check the current IRS exemption, because the numbers adjust from year to year.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

Setting up a Trust creates the container for the assets, and funding it is how the assets actually get into the Trust.

A Revocable vs. Irrevocable Trust comes down to one trade-off: control versus protection. Revocable lets you stay in the driver's seat. Irrevocable moves your assets somewhere creditors and estate taxes can't easily reach.

A partition action can help give you a path forward when you just can’t agree with a property co-owner — even if you’ve reached a stalemate.