Personal Property

6 min read

Heirs vs. Beneficiaries: Who Inherits a Loved One's Estate?

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

Trusts and estates aren’t directly comparable. An estate is the property and debts someone has when they pass away. Everyone has an estate. A Trust is a legal instrument that helps transfer property within an estate.

Thinking about what happens to your belongings after you're gone isn't easy, but planning ahead is one of the best things you can do for your family. Estates are complicated, and they’re resolved according to a combination of state law and documents that you leave, like your Will.

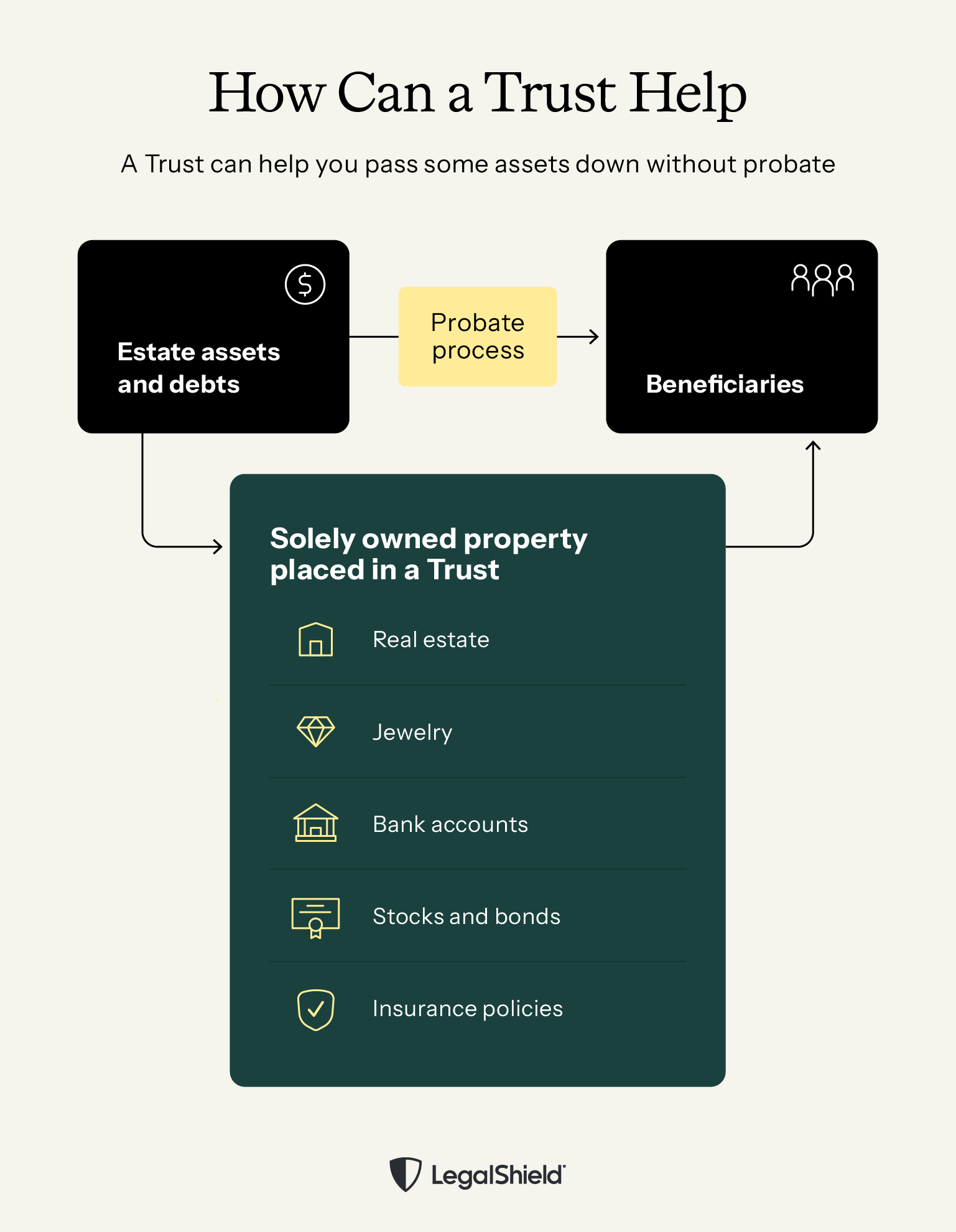

A Trust is like a bridge between a person and their estate. A Trust can make it easier for your family to manage your estate when the time comes. In some cases, setting up a Trust lets estate property transfer without going through probate.

An estate is everything someone owns when they die, minus any debts and liabilities. Everyone has an estate, and there are laws governing how estates get handled. An estate can include property like these items:

The probate process is required to oversee the determination of an estate. This includes using estate property to pay a deceased person’s bills and other debts. The probate court also oversees the distribution of the remaining property to heirs as instructed by the deceased’s Will.

If there’s no Will, the probate court uses the state’s intestate laws to decide how to distribute the property. You can sometimes avoid the probate process (or have an estate go through it more quickly) with the help of a Trust.

A Trust is a legal arrangement to benefit someone else by transferring property. You can better understand how a Trust works by knowing its four basic components:

Unlike an estate, a Trust only exists when someone deliberately creates one. It’s one of several tools available when creating an estate plan and doesn’t replace the estate itself. If property is placed in a Trust, it usually avoids probate.

There are three general ways that your representatives will manage your estate:

Everyone should create a Will, and often, a Will is enough to execute your estate. But there are times when your Will on its own may not be enough to take care of your family in exactly the way you want. Trusts can be useful when dealing with these situations:

Planning for the future isn’t easy and can involve difficult decisions. If you’re thinking about preparing a Will or setting up a Trust, it helps to know as much about estate planning as possible.

Our legal plans give you access to provider lawyers who can answer your legal questions. They can also help you prepare a Will or, with a Premium Plan, a Trust. They’ll also confirm that these documents comply with state-specific laws. Learn more about our LegalShield Personal Plans today.

Content Specialist at LegalShield, creating educational resources about legal and consumer protection topics. She focuses on making complex legal and financial concepts accessible to readers and has contributed to various educational articles on consumer rights and protections.

The distinction between an heir and a beneficiary is particularly important because they may receive estate assets in different ways.

For many spouses, a postnup is simply about preventing confusion and making shared decisions before money questions get harder to discuss.

You might need your deed when you’re selling your home, adding a spouse to the deed, checking ownership, or trying to settle estate questions.

The difference between "per stirpes" and "per capita" can be confusing. They sound alike and both have to do with who inherits your assets if a named beneficiary dies. We'll explain the difference.

Signing as a POA Agent is more than just jotting down your signature. Banks, title companies, healthcare providers, and similar entities might reject documents if the signature doesn’t clearly show that you’re signing for the other person.

Probate can take time, add costs, and create extra work for loved ones during an already difficult time. That’s why people often want to know how to avoid it.